By JBizNews Desk

NEW YORK, May 24, 2026 — For decades, one rule defined global finance during geopolitical crises: when war broke out, investors bought U.S. Treasury bonds.

That rule is now being tested in ways Wall Street has not seen in a generation.

Instead of rallying during the Iran conflict, the Treasury market has sold off sharply. Bond prices have fallen, yields have surged, and the world’s largest safe-haven asset class is suddenly behaving less like a shelter and more like an inflation trade.

The reason is straightforward but deeply consequential: investors no longer fear recession first. They fear inflation first.

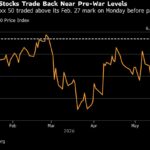

The 10-year U.S. Treasury yield, the benchmark interest rate underpinning nearly every major borrowing cost in the American economy, climbed to roughly 4.60% this week after briefly touching a 16-month high near 4.7%. Since the Iran war escalated in late February, yields have risen approximately 70 basis points — an unusually large move for sovereign debt markets.

Historically, wars triggered the opposite reaction. Investors typically fled into Treasuries during global instability, pushing yields lower as bond prices rose. That relationship held through the Gulf War, the Iraq invasion, the September 11 attacks, the European debt crisis, and much of the pandemic era.

This time, the inflation shock is overpowering the traditional safety trade.

Energy markets sit at the center of the disruption. A substantial share of global oil and fertilizer shipments move through the Strait of Hormuz, and continued instability surrounding the corridor has amplified fears of prolonged supply disruptions and structurally higher energy costs.

The economic consequences are already spreading globally. Airlines across Europe have reduced or rerouted flights due to elevated fuel costs and regional security concerns. American consumers have spent tens of billions more on gasoline this year compared with prewar expectations. Agricultural markets across Asia are dealing with rising fertilizer uncertainty that could ultimately feed back into global food inflation.

Every one of those pressures flows into the same market calculation: persistent inflation reduces the Federal Reserve’s ability to lower interest rates.

That concern is now clearly visible in inflation-expectation markets. The one-year Treasury breakeven inflation rate has climbed above 3%, while medium-term inflation expectations remain materially above the Federal Reserve’s formal 2% target.

Translated into everyday terms, bond investors increasingly believe the inflation environment of the early 2020s is not fully gone.

That matters far beyond Wall Street.

The 10-year Treasury yield directly influences mortgage rates, auto financing, corporate borrowing costs, commercial real estate lending, and the federal government’s own debt-service expenses. When yields rise and remain elevated, borrowing costs throughout the economy reset higher.

The housing market has already absorbed much of the impact. Freddie Mac’s average 30-year mortgage rate has remained above 7% for most of 2026, contributing to one of the slowest housing turnover environments in years. Home affordability has deteriorated sharply, refinancing activity has collapsed, and existing homeowners remain reluctant to sell properties tied to older low-rate mortgages.

The Federal Reserve has also become increasingly constrained.

Minutes from the Fed’s latest policy meeting showed policymakers remain concerned that inflation could reaccelerate if energy prices remain elevated through the second half of the year. Interest-rate futures markets now reflect rising expectations that the central bank may need to maintain restrictive policy longer than investors anticipated only months ago.

At the start of 2026, traders debated how quickly the Fed might begin easing. The conversation has shifted toward whether another rate increase could eventually become necessary.

The pressure extends beyond inflation alone.

Governments worldwide are issuing record amounts of debt at the same moment central banks are no longer acting as dominant buyers. According to OECD estimates, member governments issued roughly $17 trillion in sovereign debt during 2025, with issuance expected to rise further in 2026. U.S. federal debt has now crossed $39 trillion.

That creates a structural supply problem inside global bond markets: more debt must be absorbed by private investors precisely when inflation uncertainty is increasing the compensation investors demand to hold long-duration bonds.

Foreign reserve managers are also behaving differently than in past crises.

For much of the modern era, geopolitical instability automatically strengthened demand for U.S. Treasuries and the dollar. While the dollar remains dominant globally, reserve diversification has accelerated in recent years. Gold prices have repeatedly reached record highs during the Iran conflict, while several foreign central banks have gradually reduced reliance on long-dated U.S. government debt.

China’s sovereign bond market, notably, has remained comparatively stable during the conflict, underscoring how fragmented global capital flows have become compared with prior decades.

Markets increasingly view the path of oil prices as the key variable determining whether Treasuries can stabilize.

President Donald Trump has repeatedly argued that a negotiated Iran framework capable of restoring normal energy flows through Hormuz would rapidly ease inflation pressures. Administration officials have signaled that discussions remain active, though no finalized agreement has yet emerged.

If energy prices retreat materially, inflation expectations could ease and Treasury markets may begin behaving more traditionally again, with yields stabilizing or falling as geopolitical risk subsides.

If not, bond investors appear increasingly willing to price a world defined by structurally higher inflation, tighter monetary policy, and permanently elevated borrowing costs.

What makes the moment historically significant is not simply the Iran war itself.

It is the possibility that the foundational assumption underpinning modern finance — that U.S. Treasuries automatically function as the ultimate global refuge during crises — is no longer operating as reliably as it once did.

For now, the bond market’s message is clear: inflation risk has become powerful enough to overpower fear itself.

JBizNews Desk

© 2026 JBizNews. All Rights Reserved. Reproduction or distribution without written permission is prohibited.