Baseline

Remember the empty streets, boarded up stores, and bare shelves of 2020? Something like that appears highly likely, should there not be any major positive developments in the Middle East (which looks quite unlikely).

Luckily, rather than guessing, we can look at hard data and actual numbers:

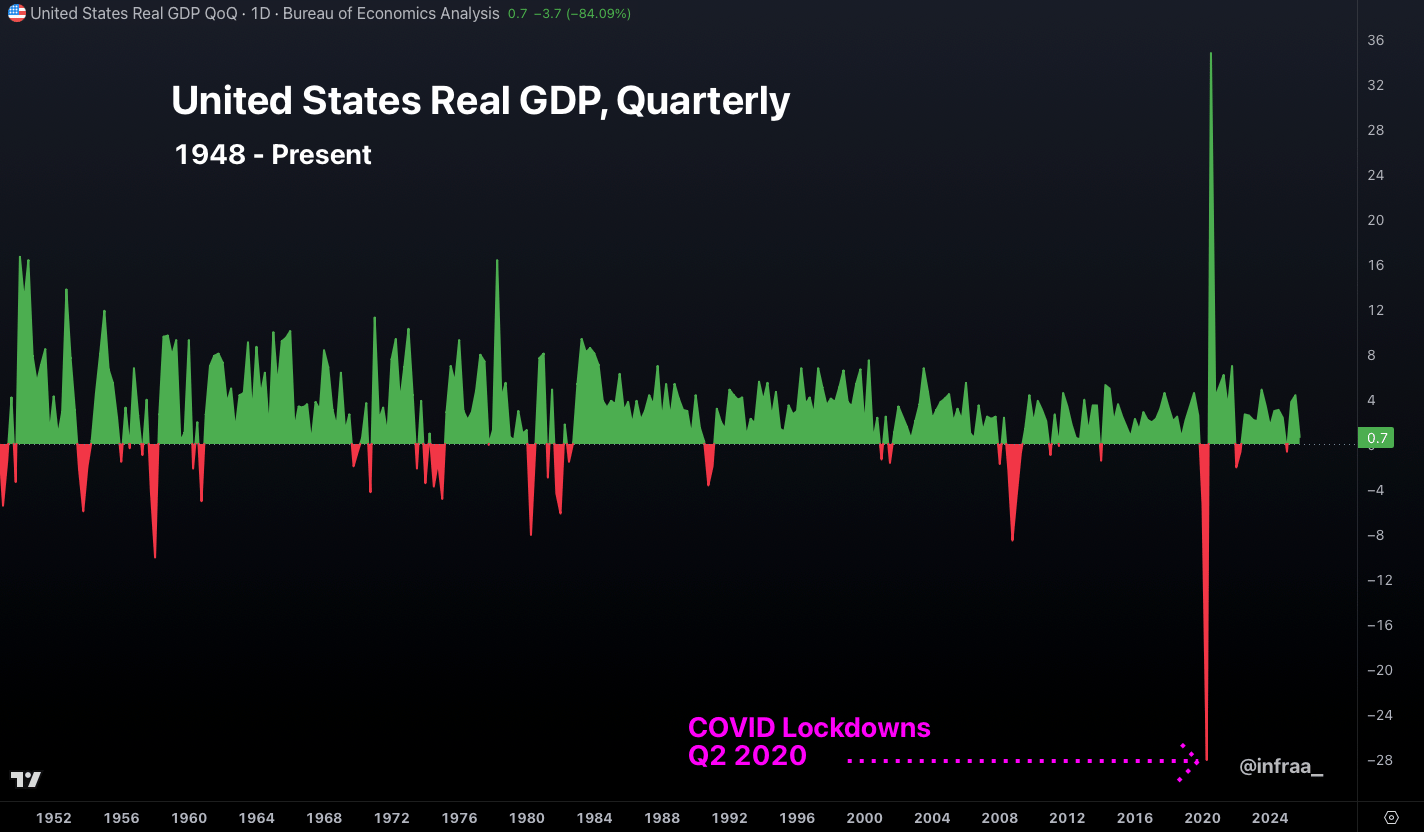

During the 2nd quarter of 2020, the global economy came to a screeching halt. Freeways empty, shipping halted, bare shelves, closed up shops and ‘non-essential worker’ lockdowns.

According to the Bureau of Economic Analysis’s Q2 2020 GDP print, the US economy shrank by 32%, just in Q2 alone. A third of the US economy- gone.

Because COVID was such a rapid & unexpected shock, there was a huge imbalance between the supply of oil and the demand for it.

This is the sort of economic collapse that was required to destroy the demand for oil. All in all, during Q2 of 2020 (height of the COVID lockdowns), demand for oil fell by 23 million barrels per day (‘bpd’).

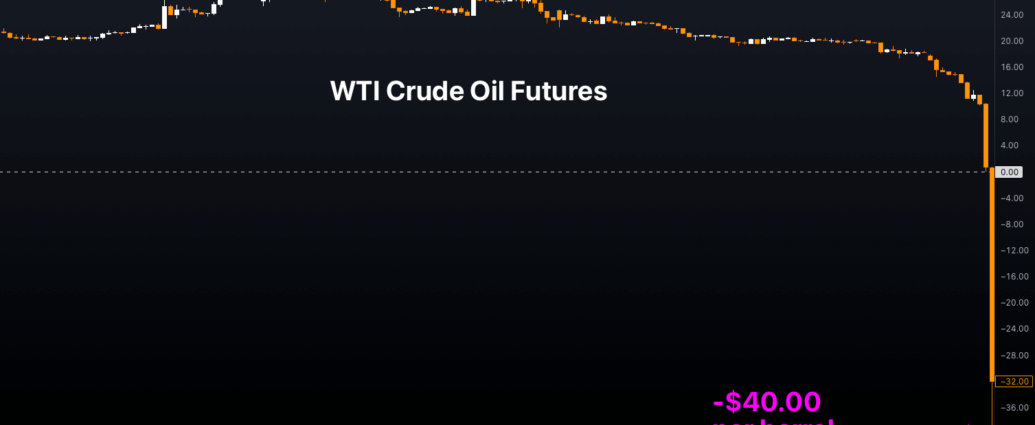

Given that the clearing mechanism for such an imbalance between supply and demand is price, oil prices famously had to go to -$40 to clear the market.

Negative $40 per barrel. That was what was required to clear the 23 million bpd loss of demand due to the global economy screeching to a halt.

So what about today? What’s the situation now?

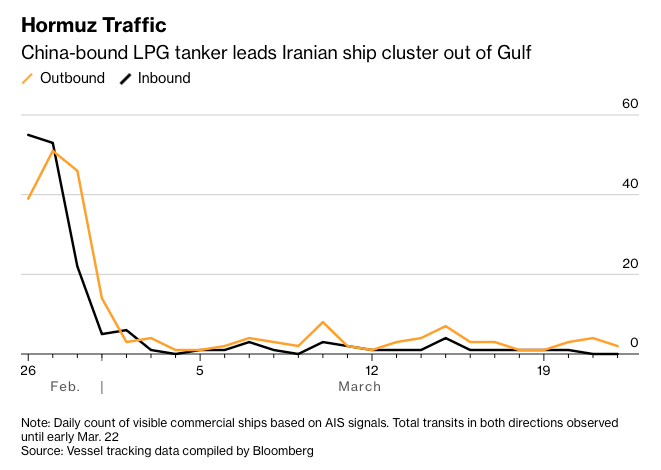

The Strait of Hormuz, which normally carries about 20 million barrels per day of crude oil and products (according to the IEA), is effectively closed. There is no physical blockade (though there may be mines)- but the strait is effectively closed with traffic down 97% and 20 million barrels of oil taken offline.

20 million barrels of oil supply were taken offline, just from this one chokepoint. Remember, supply = demand (with prices as the clearing mechanism).

But we didn’t just see a supply reduction from the Strait- you need to store oil somewhere. This is called “inventories.”

Due to the outbound flow being stopped, refineries started filling inventories. When the tanks fill …

This post was originally published here