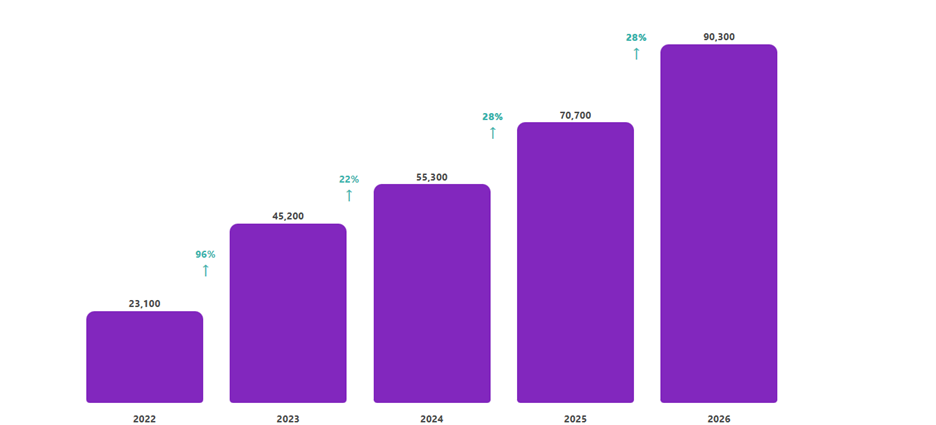

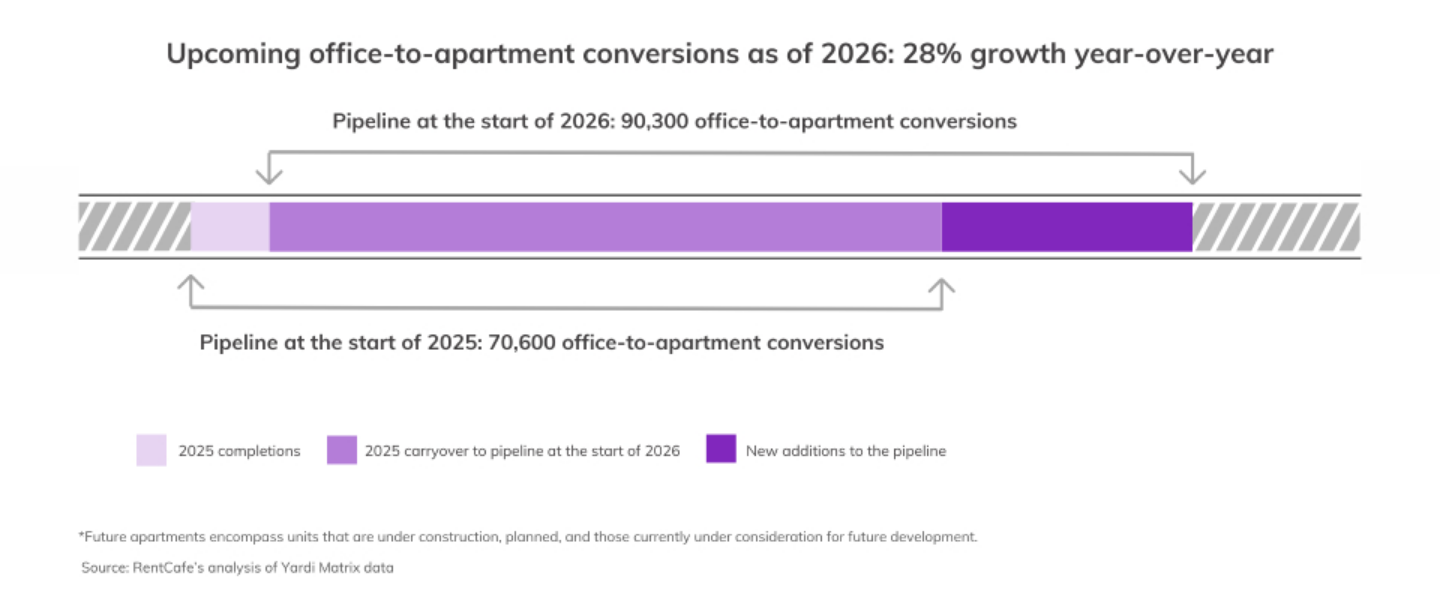

A record 90,000 apartments are now in the U.S. pipeline of office-to-apartment conversions, according to RentCafe’s latest analysis of Yardi data – a sign that each year shifts adaptive reuse even more from niche strategy to mainstream development tool. The surge comes as office vacancy persists under hybrid work and housing demand remains strong in supply-constrained cities.

“Office-to-residential conversions are no longer just a workaround for distressed buildings – they’re becoming a strategic tool for adding housing in supply-constrained markets,” said Doug Ressler, senior analyst and manager of business intelligence at Yardi Matrix.

A FAST-GROWING PIPELINE FUELED BY MARKET SHIFTS

The rise in conversions reflects two key trends coming together: higher office vacancy rates and an ongoing need for more housing. As companies reassess how much space they need, some office buildings – particularly older ones – are seeing lower demand. At the same time, renters continue to face limited housing options in many desirable urban locations.

This imbalance is creating opportunities for developers to reposition office assets into residential units. Compared to ground-up construction, conversions can offer a faster path to delivery in well-located areas where zoning and land availability might otherwise slow new development.

Still, not every building is a good candidate. “The feasibility of office conversions depends heavily on building design – factors like floor depth, window access and structural layout can make or break a project,” explained Peter Kolaczynski, director of data and research at Yardi.

Most conversion activity is concentrated in properties built between the 1960s and 1990s, which tend to have layouts better suited for residential use.

WHY OLDER OFFICE BUILDINGS ARE LEADING THE WAY

A defining feature of the current conversion wave is the age of the buildings involved. Most projects focus on offices that are already several decades old – not because they are outdated in every sense, but because their design makes them easier to adapt.

Older buildings typically have narrower floor plates, which allow more units to access natural light – a key requirement for residential use. They also often feature operable windows and structural layouts that simplify reconfiguration.

By contrast, newer office buildings tend to have deeper floor plans and large glass facades, which can complicate residential conversions. In many cases, these properties are better suited for continued office use or full redevelopment rather than conversion.

In practice, not every office building can be converted. Even as more projects move forward, only certain properties have the right layout and features to make the switch to residential use.

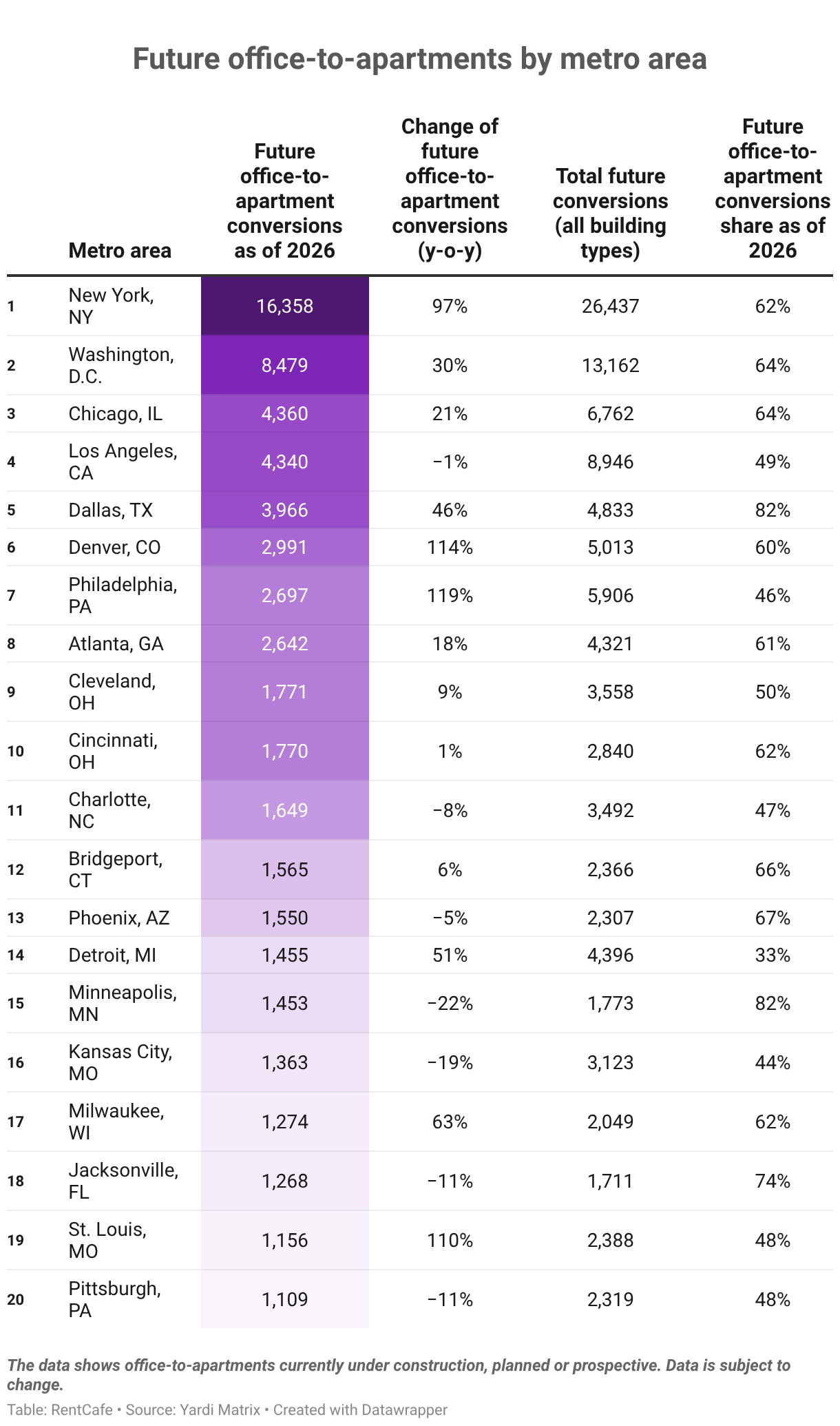

NEW YORK CITY LEADS, BUT ACTIVITY IS SPREADING NATIONWIDE

New York City leads the office-to-apartment conversion landscape, with the largest pipeline of units nationwide in 2026: over 16,000 units. A combination of older office stock, strong demand for rental housing, and supportive policy changes has helped position the city at the forefront of adaptive reuse.

But the trend is no longer limited to coastal gateways. Cities across the Midwest and South are increasingly embracing conversions to reinvigorate downtown areas and add housing without relying solely on new construction.

Chicago and Cleveland, for example, are making use of historic office buildings to bring residents back into their urban cores. Washington, D.C., is another key player, supported by local incentives aimed at encouraging office repositioning. Meanwhile, Los Angeles is seeing steady activity, particularly in its downtown area.

Smaller metros are also embracing the trend. In these markets, conversions can play a key role in revitalizing central business districts that have seen reduced foot traffic in recent years.

POLICY SUPPORT HELPS CLOSE THE GAP

Office conversions can be complex and costly, often requiring significant upgrades to meet residential building codes and tenant expectations. That’s where policy support comes into play.

Cities across the country are introducing zoning changes, tax incentives and streamlined approval processes to encourage adaptive reuse. New York City, for instance, has expanded eligibility for office-to-residential conversions, opening the door for more projects. Washington, D.C., has implemented financial incentives aimed at jumpstarting activity.

These measures are helping bridge the financial gap that can make conversions challenging, particularly in markets where construction costs remain high.

At the same time, public-private collaboration is becoming increasingly important. By aligning development goals with housing needs, cities can use conversions as a tool to address both office vacancies and housing shortages.

CHALLENGES PERSIST, BUT MOMENTUM IS BUILDING

Despite its growth, the conversion trend still faces limitations. Structural constraints, financing hurdles and high construction costs can all impact project feasibility. In some cases, developers may find that only a portion of a building can be converted, or that costs outweigh potential returns.

Even so, as office demand stabilizes at lower levels and housing needs remain pressing, conversions are likely to remain part of the development mix.

Beyond adding units, these projects also contribute to more balanced urban environments. They help bring residents into office-heavy districts and support local businesses by attracting increased foot traffic and creating more active neighborhoods.

A PRACTICAL PATH FOR ADDING HOUSING

Office-to-apartment conversions are not a silver bullet for the housing shortage, but they are becoming an increasingly practical solution in the right contexts. For developers, they offer a way to reposition underperforming assets. For cities, they provide a strategy to breathe new life into downtown areas. And for renters, they expand housing options in locations that might otherwise see little new supply.

For more insights, charts and a detailed methodology, read the full report on RentCafe.com.