Loan officer mobility is continuing to decline even as the overall pool of active producers rebounds from recent low points. This appears to signal a shift in how originators are weighing risk, compensation and opportunity, according to a recent mortgage market intelligence report from RETR.

Loan officer movement has long served as a proxy for confidence in the industry. When originators believe they can grow their business, they’re more likely to switch platforms or pursue better economics. But data from RETR suggests that the dynamic is cooling.

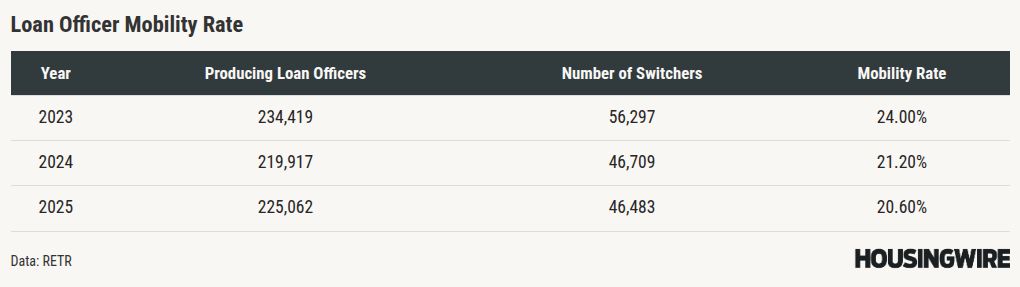

In 2023, out of 234,419 producing loan officers, 56,297 switched companies, a mobility rate of about 24%. In 2024, production fell to 219,917 LOs, with 46,709 switching firms, lowering the mobility rate to 21.2%.

By 2025, the number of producing LOs rebounded to 225,062, but only 46,483 changed companies, pushing mobility down further to a rate of 20.6%.

The decline in mobility has persisted even as the market stabilizes, suggesting the slowdown is not purely a function of fewer originators but reflects broader structural factors.

“Loan officers are staying put because stability matters more than ever. Most are prioritizing consistent deal flow, strong support and trusted referral networks over chasing marginal comp differences,” RETR’s James Hooper told HousingWire. “As the market recovers, they’re doubling down on platforms and companies that help them retain clients and generate repeat business rather than starting from scratch elsewhere.”

RETR points to a “wait and see” environment, where loan officers are less willing to absorb the operational disruption of a move unless the upside outweighs it. At the same time, compensation compression across lenders has reduced differentiation, making platforms appear more similar from an earnings perspective.

Despite retention efforts by top lenders — including technology investments, support infrastructure and targeted incentives that appear to be keeping more originators in place — lower mobility does not necessarily signal higher satisfaction.

Performance data on loan officer “movers” adds additional context. A separate RETR analysis of roughly 26,000 active LOs who switched companies in 2024 found that their average loan volume rose from $8.33 million in 2023 to $10.18 million in 2025 — a 22% increase. Average loan counts increased from 24 to 28 units, up 17%.

But RETR pointed out that these gains closely tracked broader market trends. Total mortgage volume rose from $1.69 trillion in 2023 to $2.03 trillion in 2025, a 20% increase, while total loan counts grew 9% to 5.87 million.

The dataset excludes roughly 20,000 loan officers who left the industry, focusing only on those still active in 2026, a factor that likely skews the group toward higher-performing originators.

Weekly movement data underscores the continued slowdown in mobility, even as some originators continue to change firms. According to RETR’s newest weekly data, 284 loan officers switched companies, while 1,285 individuals obtained new licenses through the Nationwide Multistate Licensing System (NMLS).

Recent notable moves included Jonathan Esposito ($121.5 million, 289 units) joining Atomic Mortgage LLC; Steven Crawford ($111.9 million, 222 units) moving to HomeAmerican Mortgage Corp., and Arya Bybordi ($103.5 million, 389 units) joining United Lending Team Inc.

On the company side, several nonbank lenders posted gains based on aggregated loan officer production over a 14-month period. Integrity Home Mortgage Corp. led with a 17.28% increase, followed by Atlantic Avenue Mortgage LLC at 16.84% and Mortgage Solutions FCS Inc. at 8.39%.