A growing number of American homeowners are making a stark financial calculation: as insurance premiums surge to levels many can no longer afford, they are choosing to go without coverage altogether — leaving themselves exposed to potentially catastrophic losses when disaster strikes.

The shift is no longer isolated. Housing and insurance analysts say the trend is accelerating nationwide as the home insurance market undergoes a structural transformation driven by the rising frequency and severity of extreme weather events. From wildfires in California to hurricanes in the Southeast and hailstorms across the Midwest, insurers are facing mounting claims exposure — and responding by pulling back.

“The market is fundamentally repricing risk,” said Mark Friedlander, Director of Corporate Communications at the Insurance Information Institute, noting that carriers are increasingly exiting high-risk regions, sharply raising premiums, tightening underwriting standards, or limiting coverage altogether. “In many areas, the traditional model is breaking down.”

For homeowners, the consequences are immediate and severe. Policies that once cost a few thousand dollars annually are now doubling or tripling in certain markets, pushing coverage out of reach for middle- and lower-income households. In some cases, insurers are declining to renew policies entirely, leaving homeowners with no viable alternatives.

The result is a growing “coverage gap” — a divide between those who can afford protection and those who cannot.

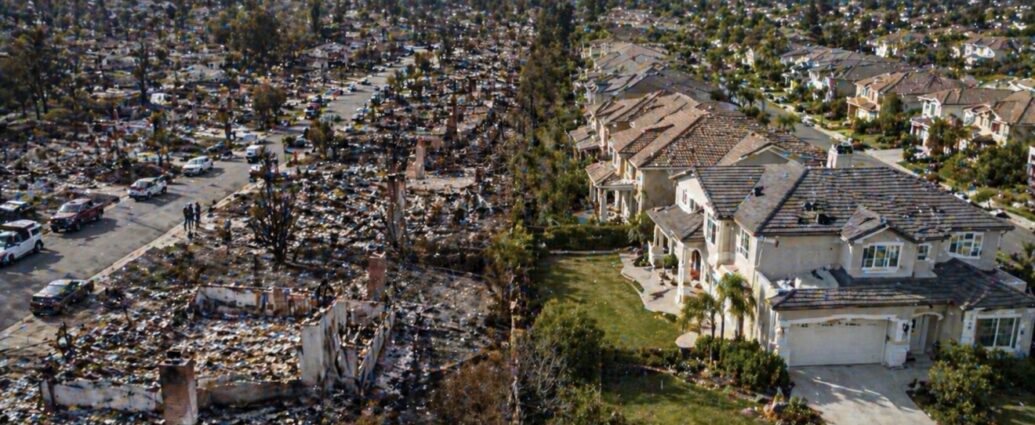

That divide is becoming visible on the ground. In the aftermath of California’s January 2025 Eaton Fire, aerial surveys revealed entire neighborhoods where some homes were rebuilt while others remained vacant lots — a stark reflection of who had insurance and who did not. For families without coverage, the loss is often permanent, wiping out what for many represents their largest source of wealth.

The ripple effects extend far beyond individual households. Mortgage lenders typically require insurance as a condition of financing, meaning uninsured or uninsurable properties can become effectively unsellable. Analysts warn that this dynamic could begin to suppress home values in high-risk areas, while also eroding local tax bases that depend on property assessments.

“This is not just a housing issue — it’s a financial stability issue,” said one real estate economist. “If insurance becomes unavailable, entire markets can start to freeze.”

At the same time, the scale of weather-related losses continues to climb. The Insurance Information Institute estimates that severe storms alone generated $51 billion in insured losses last year, a figure that does not account for the full economic damage borne by uninsured households. As climate-related risks intensify, those losses are expected to rise further.

The crisis is also intersecting with growing legal scrutiny of the insurance industry. A wave of lawsuits — including high-profile cases involving State Farm — alleges that some carriers have sought to minimize payouts even when coverage exists, further undermining confidence in the system. Insurers have denied wrongdoing, but the litigation adds another layer of uncertainty for homeowners already questioning whether their policies will deliver when needed.

For policymakers, the challenge is becoming urgent. Consumer advocates and state regulators are increasingly calling for structural reforms, including expanded state-backed insurance programs, risk-sharing mechanisms, and updated regulatory frameworks to stabilize markets.

“The current trajectory is unsustainable,” said one state insurance regulator, warning that without intervention, the number of uninsured homes could continue to rise sharply.

What emerges is a fundamental shift in how risk is distributed across the American housing system. Where insurance once served as a reliable financial safety net, it is increasingly becoming a privilege — available to those who can afford it, and out of reach for those who cannot.

Unless the gap is addressed, the next major disaster will not just test infrastructure — it will expose, in real time, how fragile the nation’s housing safety net has become.

JBizNews Desk