Walk Forward Analysis is one of the most widely used techniques in systematic trading for strategy validation and for reducing the risk of overfitting.

Testing trading strategies that have performed well in the past is actually quite simple: it is enough to find a set of rules that fits historical data. The problem is that, by doing so, we inevitably tie the system to that specific dataset, and as a result, it is unlikely to have real predictive power.

At this point, it is important to remember that a trader’s goal is not to satisfy their ego by building a strategy that perfectly “explains” the past, but to develop a model capable of producing results in the future.

For this reason, a variety of validation methods have been introduced over time, designed to make the transition from past performance to future results more realistic and less prone to misleading conclusions. Among these, Walk Forward Analysis stands out as one of the most widely recognized validation techniques.

How Walk Forward Analysis Works: In-Sample and Out-of-Sample

Walk Forward Analysis is a validation technique designed to simulate, as realistically as possible, the process through which a trading strategy is developed and applied over time.

The methodology behind Walk Forward Analysis is based on two key concepts: in-sample (IS) and out-of-sample (OOS). The in-sample period is used to build and optimize the strategy, meaning to select the best-performing parameters. The out-of-sample period, on the other hand, consists of data that was not used during optimization and serves to evaluate how the strategy performs under new conditions.

To make this more concrete, imagine optimizing a parameter, such as the length of a moving average, over the period 2010–2015. Once the “best” value is identified, it is then tested on the following period, for example 2016–2017. This represents a classic out-of-sample test.

Walk Forward Analysis extends this approach by repeating the process multiple times over different time windows: the strategy is optimized on a historical segment, then tested on the subsequent period using the selected parameters, after which the entire window is shifted forward and the process is repeated. In this way, instead of relying on a single out-of-sample phase, we obtain a sequence of out-of-sample tests which, when combined, form an equity curve that more closely reflects what could have happened in real trading conditions.

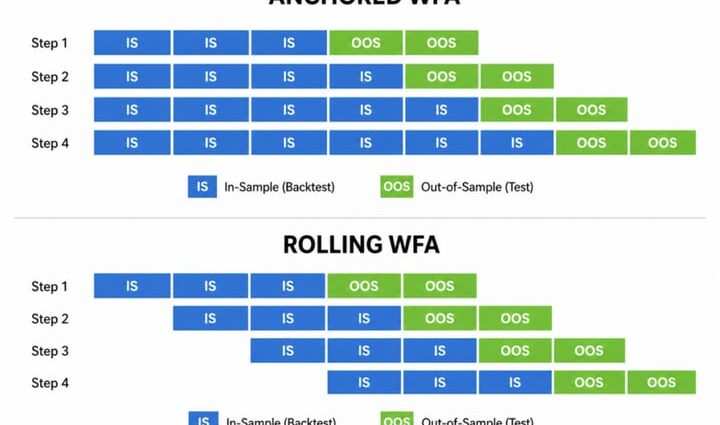

Anchored vs Rolling Walk Forward Analysis: Key Differences

There are two main ways to implement this process: anchored and rolling. As shown in Figure 1, in the anchored approach the in-sample period progressively expands over time, while in the rolling approach a fixed-length window is used and moved forward …

This post was originally published here