The economics of America’s booming weight-loss-drug market have been fundamentally rewritten after the Trump administration’s “Most Favored Nation” pharmaceutical pricing deals pushed the cost of blockbuster GLP-1 medications sharply lower for millions of Americans, including Medicare beneficiaries receiving obesity treatment for the first time.

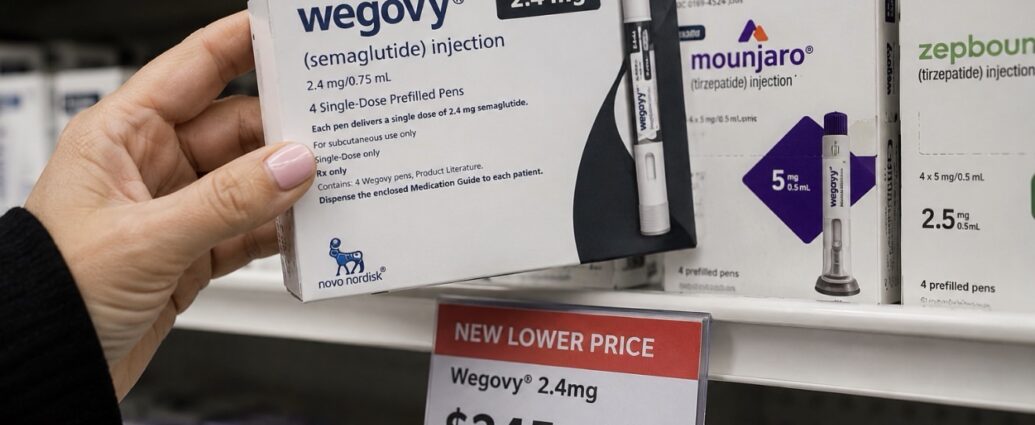

Under the new framework now taking effect nationwide, eligible Medicare patients can access Wegovy, Ozempic, Zepbound and Mounjaro for roughly $245 per month, with many beneficiaries paying co-pays closer to $50 monthly depending on plan structure and supplemental coverage.

The pricing reset marks one of the largest structural changes to U.S. pharmaceutical pricing in decades and dramatically expands access to a category of drugs that has rapidly become one of the most important stories in healthcare, consumer behavior and even the broader economy.

Before the agreements, many patients without comprehensive insurance coverage faced annual out-of-pocket costs exceeding $13,000 for GLP-1 medications.

The Trump administration’s Most Favored Nation agreements with Eli Lilly and Novo Nordisk, signed in late 2025, effectively forced a broad restructuring of pricing across obesity and diabetes medications while opening the door for Medicare obesity coverage tied to related health conditions.

The impact on consumers is immediate.

Lilly’s obesity drug Zepbound, which previously carried a list price above $1,000 per month, is now available through direct-to-consumer and government-linked programs at dramatically reduced pricing depending on eligibility and dosage.

Novo Nordisk’s Wegovy and Ozempic now fall under similar pricing frameworks through Medicare and participating distribution platforms.

The administration also launched the new TrumpRx platform, designed to centralize lower-cost access to medications participating in the pricing framework.

Under the system, certain obesity drugs, diabetes therapies and chronic-disease medications now carry prices far closer to international benchmarks than historic U.S. list prices.

The structural Medicare change may prove even more important than the pricing itself.

For years, Medicare Part D rules effectively prohibited broad coverage of anti-obesity medications under restrictions dating back to the 2003 Medicare Modernization Act.

The administration’s legal interpretation now allows coverage when obesity is paired with recognized related conditions such as cardiovascular disease, diabetes, sleep apnea or metabolic disorders.

That dramatically expands the eligible patient pool.

Medicare currently covers roughly 65 million Americans, with analysts estimating that between 15 million and 25 million beneficiaries may qualify for GLP-1 therapy under the revised framework.

State Medicaid programs are also beginning to adopt similar structures, with multiple states already approving expanded obesity-drug access.

The shift is creating winners and losers across the pharmaceutical industry.

Eli Lilly appears best positioned.

The company continues dominating the injectable obesity market through Zepbound and Mounjaro while simultaneously expanding into oral GLP-1 therapies with newly approved Foundayo.

Lilly executives have acknowledged that pricing pressure will reduce per-unit economics but argue that dramatically higher patient volume will offset much of the revenue impact.

Novo Nordisk faces a more complicated transition.

The Danish pharmaceutical giant still controls massive global scale through Wegovy and Ozempic but has warned investors that pricing resets and future patent expirations are likely to pressure growth over the next several years.

The effects extend well beyond pharmaceutical manufacturers themselves.

Retail pharmacy chains including CVS Health and Walgreens Boots Alliance are positioned to benefit from increased prescription volumes, while employers and insurers could eventually see downstream healthcare savings tied to lower obesity-related complications.

The broader economic implications are increasingly difficult to ignore.

GLP-1 medications have already begun reshaping spending patterns across food, apparel, fitness, healthcare and consumer sectors as weight loss and metabolic improvements alter behavior for millions of users.

Analysts now estimate the broader GLP-1 category could eventually exceed $150 billion in annual global sales, making it one of the largest pharmaceutical markets in modern history.

Critics of the administration’s pricing structure, however, remain vocal.

Several Democratic senators — including Elizabeth Warren, Bernie Sanders, Amy Klobuchar and Jeff Merkley — have demanded additional details regarding implementation, pricing formulas and interactions with existing federal drug-pricing programs.

Questions also remain about the long-term durability of the framework and the legal challenges likely to emerge from portions of the pharmaceutical industry.

Still, for patients standing at the pharmacy counter today, the practical reality is already clear.

A category of medications once viewed as financially inaccessible for much of the middle class is rapidly becoming mainstream healthcare.

The GLP-1 market is no longer a niche obesity-treatment story confined to wealthy consumers or celebrity culture.

It is becoming one of the largest and most politically consequential healthcare shifts in modern American medicine.

JBizNews Desk

© JBizNews.com. All rights reserved. This article is original reporting by JBizNews Desk. Unauthorized reproduction or redistribution is strictly prohibited.