By JBizNews Desk

WASHINGTON — June 1, 2026

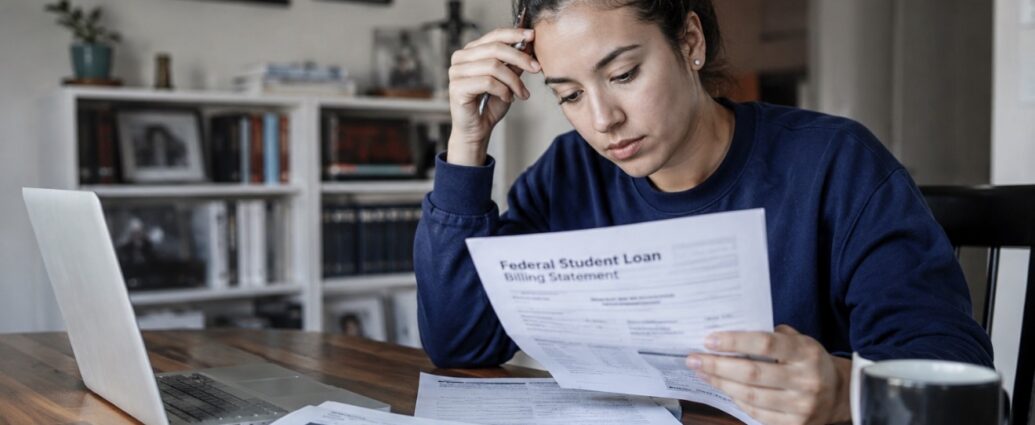

Millions of students and parents are facing a major change in how federal student loans work, and the deadline is fast approaching.

Beginning July 1, 2026, anyone taking out a new federal student loan will enter a significantly different repayment system than borrowers who took out loans before that date. Financial advisers say the changes could affect monthly payments, loan forgiveness opportunities, and how much families can borrow for college.

The new rules stem from the One Big Beautiful Bill Act, signed into law in 2025, and represent one of the most substantial overhauls of federal student lending in years.

“This is really high-stakes stuff,” said Kathleen Boyd, a certified financial planner and founder of Student Loan Savvy. She warns that many borrowers may not realize how dramatically the system is changing.

For years, federal student loan borrowers could choose from a variety of repayment plans based on income, career path, and financial circumstances. Beginning July 1, most new borrowers will have only two choices: the Repayment Assistance Plan (RAP) and a new Tiered Standard Repayment Plan.

The distinction between old and new borrowers could have long-term consequences.

According to student-loan attorney Stanley Tate, borrowers who already have federal loans should be especially careful before taking out additional loans after July 1. Even a relatively small new federal loan could affect which repayment programs are available in the future.

One of the most significant changes is the loss of access to Income-Based Repayment (IBR) for new borrowers. IBR has been popular because payments adjust to income levels, some borrowers can qualify for payments as low as zero dollars per month, and loan forgiveness can occur after as little as 20 years.

Under the new Repayment Assistance Plan, borrowers generally pay between 1% and 10% of their income, depending on earnings. However, forgiveness generally comes only after 30 years, meaning many borrowers could remain in repayment for an additional decade compared with some current programs.

For families already struggling with college costs, that difference could be substantial.

Graduate students are also facing major changes.

The legislation eliminates Grad PLUS loans, which have historically allowed students pursuing advanced degrees to borrow up to the full cost of attendance. Medical students, law students, dental students, and other professional-degree candidates have relied heavily on the program for decades.

Without Grad PLUS loans, students may need to cover more of their education costs through savings, scholarships, employer assistance, or private financing.

Parents will face tighter borrowing limits as well.

Higher-education expert Mark Kantrowitz notes that new Parent PLUS loans will be capped at $20,000 per year per dependent student, with a lifetime maximum of $65,000 per student. Graduate students will generally be limited to $20,500 annually and $100,000 total borrowing, while most borrowers will face an overall lifetime federal borrowing limit of $257,500.

Supporters of the changes argue that stricter limits are necessary to curb excessive student debt and encourage colleges to control costs.

Nicholas Kent, Under Secretary of Education, said the reforms are intended to help students access higher education without accumulating unsustainable debt while encouraging institutions to address rising tuition prices.

Critics argue the opposite may occur.

Higher-education advocates warn that limiting access to federal financing could make professional degrees harder to obtain, particularly for students from lower-income households. Some also fear the changes could worsen workforce shortages in fields such as healthcare, where advanced education is often required.

The economic impact extends beyond students and families.

Graduate and Parent PLUS loans account for approximately $125 billion of America’s roughly $1.7 trillion federal student loan portfolio. As federal borrowing becomes more restricted, private lenders could see increased demand, while colleges may face greater pressure to justify tuition costs and keep programs affordable.

Financial advisers recommend that students and parents review their borrowing plans before July 1.

Experts suggest checking current federal loan balances through StudentAid.gov, reviewing how future borrowing may affect repayment eligibility, and consulting financial-aid offices about how the changes could impact the upcoming academic year.

For many Americans, July 1 will simply be another day on the calendar. For students and parents planning to borrow for college, however, it marks the beginning of a very different student-loan system—one with fewer options and potentially longer repayment obligations.

Washington — JBizNews Desk

© JBizNews.com All Rights Reserved. Reproduction or distribution without written permission is prohibited.