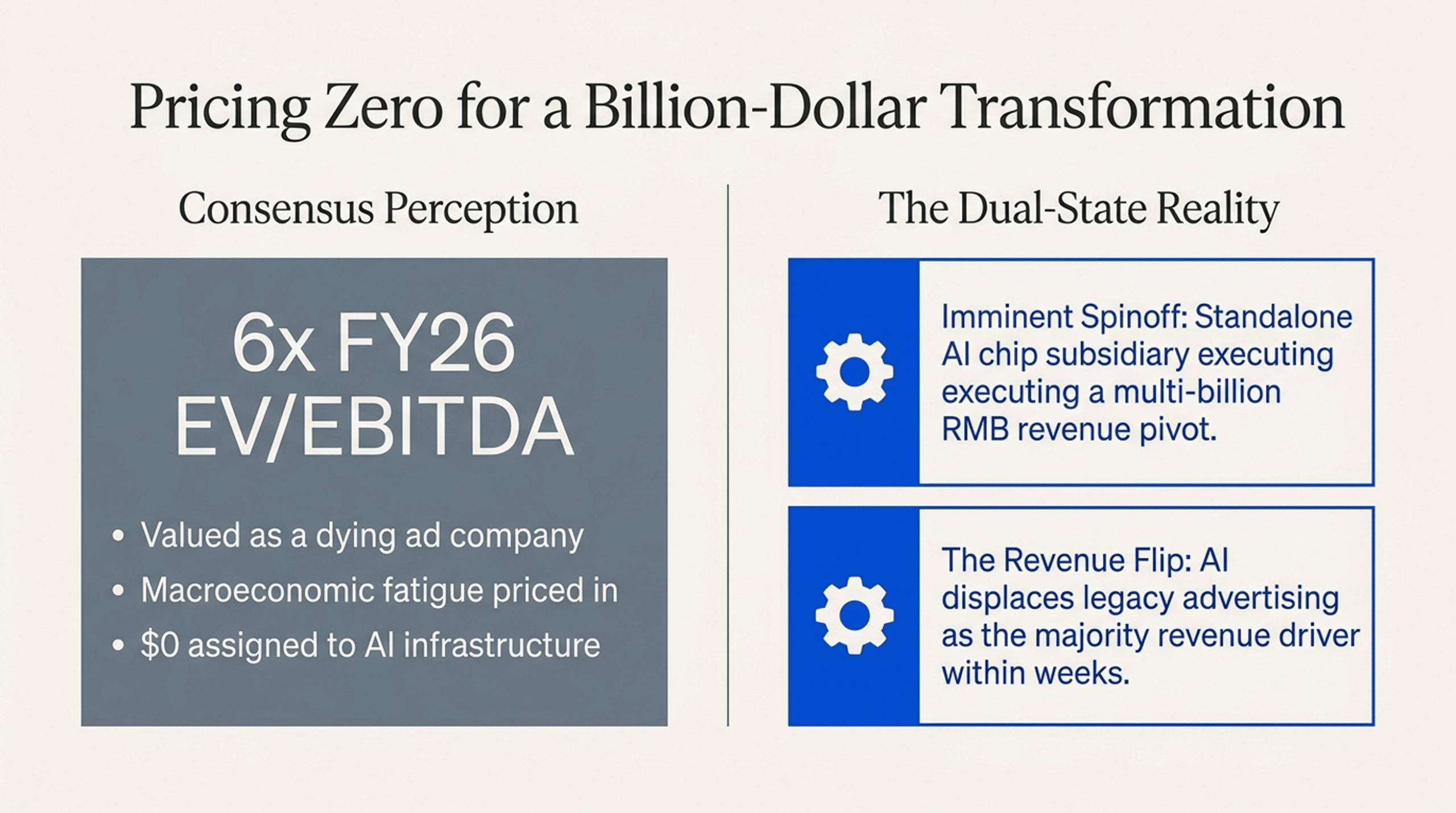

A 6x EV/EBITDA multiple. A chip business worth $9 to $13 billion that’s currently valued at zero. A revenue mix flip happening at next Q1 earnings. The math doesn’t reconcile.

This week’s Wolf Pick: Baidu

There’s a $43 billion company trading at roughly 6x EV/EBITDA, a multiple normally reserved for dying businesses. It also owns a soon-to-be publicly listed AI chip subsidiary that one major Wall Street bank values at $9 to $13 billion on its own. Q1 earnings drop May 18. A research briefing reviewed by our editorial team argues this is one of the cleanest mispricing setups in global tech right now.

The Setup the Market Is Missing

Baidu (NASDAQ:BIDU) is the company most Western investors still think of as “the Google of China.” Search bar. Ad revenue. Slow grower. Trapped in a regulatory environment nobody wants to underwrite.

That mental model is about to get destroyed by two events happening within weeks of each other.

The first is the Kunlunxin spinoff. The second is a revenue mix milestone that will mathematically reclassify what Baidu actually is. Neither is reflected in the stock at $127, and neither requires Baidu to grow faster than already projected. Both are functions of recognition, not execution.

Catalyst One: The Kunlunxin Spinoff Is Already in Motion

Most investors who follow Baidu know the company has been quietly building its own AI chips for over a decade. Very few understand what is actually happening inside that program right now.

Kunlunxin is Baidu’s AI semiconductor subsidiary. On January 1, Kunlunxin confidentially filed a listing application with the Hong Kong Stock Exchange to spin off as a standalone public company, with Baidu retaining a controlling stake. Baidu jumped 12% on the news that day.

Here is where it gets interesting. According to research circulated to institutional desks, Kunlunxin in 2024 was largely a captive supplier. Roughly 80% of its output went directly to Baidu’s own infrastructure. That model is being deliberately dismantled. Management is targeting an 80% external sales mix by 2030, with the transition already underway. External clients now include China Mobile, Tencent, and a growing list of Chinese state-owned enterprises and telecoms.

This post was originally published here