[Editor’s Note: Berkshire Hathaway‘s planned acquisition of Taylor Morrison is one of those rare transactions whose significance extends well beyond the companies involved. Today’s analysis examines the deal through a broad strategic lens, exploring why Berkshire may be betting not simply on a homebuilder, but on a leadership team, a scalable operating platform and the long-term value of an increasingly integrated housing ecosystem.

This first analysis is intended as the opening chapter in a series.

In the days ahead, The Builder’s Daily will take deeper dives into several questions this transaction raises for homebuilding, residential development and housing investment leaders: whether Taylor Morrison’s long-stated goal of reaching 20,000 annual closings signals a new minimum threshold for meaningful economies of scale; what the acquisition says about the leadership legacy of Sheryl Palmer and the strategic value of customer-centricity; whether Berkshire’s move broadens the field of likely acquirers beyond homebuilders and Japanese housing enterprises to include global capital and asset-management giants; whether the next era of competitive advantage in housing will belong to companies capable of assembling vertically integrated ecosystems that connect capital, land, manufacturing, building products, technology, distribution, insurance, mortgage finance, and homebuilding operations; and whether the deal establishes a new valuation benchmark for publicly traded builders.

Taken together, those questions may prove as important as the transaction itself. Because while Berkshire Hathaway’s acquisition of Taylor Morrison changes the ownership of one company, it may also serve as part of an emerging roadmap of where the homebuilding business is headed next.]

We’re whirling through a convective updraft of homebuilding mergers and acquisitions, one not to be outdone by the one before. Together, they upend a long-running assumption about consolidation in residential development and construction.

Who is buying whom is hardly the most compelling matter.

Rather, the question that bright-lines these multi-billion-dollar deals is exactly what capability is being acquired, along with the more obvious tangible assets. Moreover, it’s about how the acquisition at hand may be expected to cascade into an ever more concentrated balance of power in the new residential construction, development and investment arena.

This question was underscored when Sekisui House acquired MDC Holdings/Richmond American Homes; Sumitomo Forestry moved to acquire Tri Pointe Homes; and Apollo Capital-backed New Home Company (now Risewell) acquired Landsea Homes.

And in a growing number of private-builder transactions, the strategic logic extends far beyond community counts, land positions or annual closings.

The real value proposition now centers on leadership teams, operating platforms, customer relationships, net ability to convert leads to sales, local market density, access to capital, and increasingly, the ability to assemble broader housing ecosystems capable of competing in a more complex, capital-intensive, and discerning customer era.

Berkshire Hathaway‘s planned acquisition of Taylor Morrison – a seismic variation on a theme of super-power combinations in the post-pandemic era – belongs within this thematic new-rules-of-the-game progression.

Yet unlike many recent transactions, Berkshire is not entering a new business – nor, as in the case of Japan- and Canada-based acquirers, is it expanding its footprint in the U.S. as a previously unexplored geographic opportunity. Berkshire has already been here, doing that.

With the Taylor Morrison purchase, it is doubling down on a real estate and home construction empire it has spent more than two decades building.

Builder Advisor Group Founder and Chairman Tony Avila notes that Berkshire’s presence in housing dates to its 2003 acquisition of Clayton Homes, which has since grown into the dominant force in manufactured and modular housing and expanded into site-built homebuilding through a series of acquisitions.

“The question that always loomed was: given the size of Berkshire’s balance sheet and their conviction in the U.S. economy, why was their investment in residential housing so small?” Avila said. “Housing is the largest sector of the economy and Berkshire had a relatively modest allocation to the site-built segment, which represents the vast majority of new home production in this country.”

And – because of the particular blend of interests here – the deal advances this narrative. Berkshire is not merely acquiring one of America’s highest-performing homebuilders. It is making a strategic wager on a leadership team, a scalable operating platform and the long-term value of an increasingly integrated housing ecosystem.

“One of Taylor Morrison’s proven competencies under chair and CEO Sheryl Palmer’s leadership is a relatively unheralded but important one,” said Avila. “They’re exceptionally good at integrating companies into their operating systems and business culture. That’s one of the opportunities now for Berkshire Hathaway, to blend together what are extensive but separate operating units in homebuilding.”

As Berkshire Chairman Warren Buffett might have quipped, “more to come.” Viewed through that lens, the Taylor Morrison transaction may say as much about Berkshire Hathaway’s view of housing’s future as it does about Taylor Morrison’s future itself.

Veteran homebuilding analyst Dan Oppenheim describes the transaction as “a fabulous deal on both sides.”

“Berkshire is purchasing Taylor Morrison, a company with solid profitability – not hoped-for profitability, but actual profitability – and a deep land pipeline at just over one times year-end book value,” Oppenheim said. “Relative to historical transactions for a company with that profitability and land pipeline, that’s very attractive. TMHC is more than twice Tri Pointe’s size and larger than M.D.C. when it was acquired by Sekisui House.”

Avila might align more with analysts who believe Berkshire may have gotten the better deal, especially given Taylor Morrison’s margin and operational outperformance in its Q1 earnings.

Per a CNBC report, “Based on recent completed transaction multiples, the 0.9x price-to-tangible book value multiple we estimate Berkshire is paying appears low relative to recent public builder transactions,” Citizens analysts wrote.

That observation alone should command the attention of strategic leaders throughout the homebuilding industry. While the acquisition carries immediate implications for Taylor Morrison shareholders, it also raises broader questions about how long-term capital increasingly views the future of homebuilding.

Betting on people

Warren Buffett has long maintained that Berkshire Hathaway invests in people first, then in businesses.

Viewed through that lens, the acquisition can be seen as one of the strongest affirmations of Sheryl Palmer and the leadership team she has assembled over nearly two decades.

When Palmer became CEO in 2007, Taylor Morrison was hardly viewed as a future industry powerhouse. The company was emerging from the complicated integration of Taylor Woodrow and Morrison Homes as the housing market entered what would become the worst downturn in modern history.

The skepticism at the time was understandable.

Two distinct organizations with different operating cultures, customer profiles, and business approaches were being brought together just as the housing market collapsed.

Nearly 20 years later, the results speak volumes.

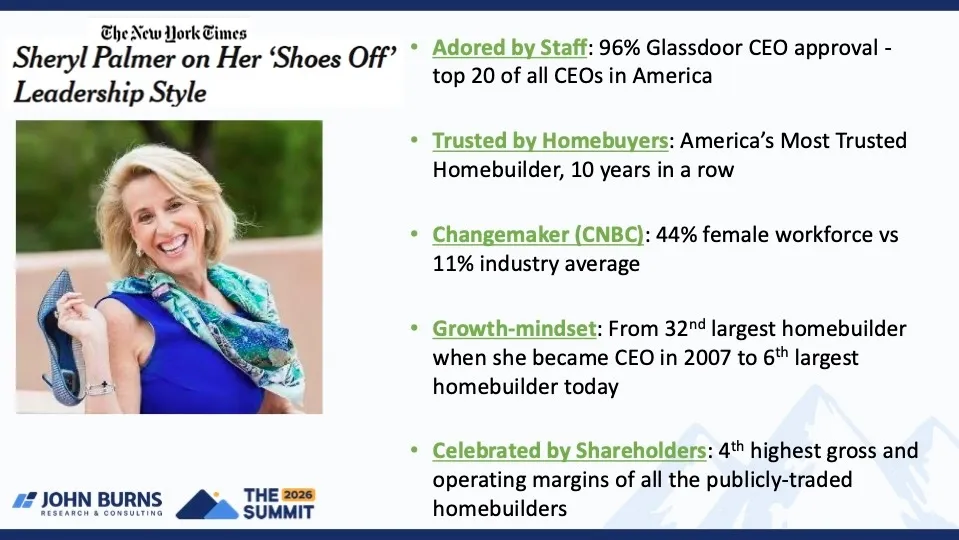

Under Palmer’s leadership, Taylor Morrison grew from the nation’s 32nd-largest homebuilder to the sixth-largest. The company earned recognition as America’s Most Trusted Home Builder for 10 consecutive years, cultivated one of the industry’s strongest workplace cultures, and consistently ranked among the top public builders by profitability.

More importantly, Palmer helped create a company whose identity centers on customer experience and trust in a sector where true consumer-facing brands remain relatively rare. Outside of Toll Brothers, few homebuilders have achieved comparable success in building positive consumer recognition at the national scale.

That achievement reflects something larger than marketing. It reflects organizational discipline. It reflects culture. And it reflects leadership.

Oppenheim believes Berkshire is acquiring a company that has been carefully positioned for long-term success. He cites Taylor Morrison’s operational improvements, financial performance, land-position discipline, and growth trajectory, including its IPO and subsequent acquisitions [AV Homes in 2018 and William Lyon Homes in 2019], as evidence that Palmer has put the company in an exceptionally strong operating and strategic position.

For Berkshire, the acquisition may represent the acquisition of one of the industry’s most effective management teams.

Betting on scale

The second layer of the investment thesis revolves around scale.

Oppenheim sees Berkshire’s capital platform helping Taylor Morrison pursue its long-stated ambition of reaching 20,000 annual closings.

Taylor Morrison’s approximately 12,000 annual deliveries, combined with Clayton’s site-built operations, effectively place Berkshire among America’s largest homebuilding enterprises. That target now takes on new meaning. Oppenheim notes that Taylor Morrison occupied an unusual position within the industry hierarchy.

“They were larger than many builders, but they weren’t in the Horton and Lennar world,” he said. “This [combination] will give them consistent capital and enable them to get to the 20,000 on their own, plus a larger platform and probably more acquisitions under the Berkshire umbrella.”

Avila sees an even larger implication.

“Taylor Morrison will add another 12,000 home deliveries to the Berkshire homebuilding enterprise, placing the combined business among the five largest builders in America,” Avila said. For an organization that has historically approached site-built housing through a collection of regional operating companies, Avila added, the acquisition creates a scaled platform that increasingly resembles a national builder’s.

The significance extends beyond Taylor Morrison itself.

For decades, homebuilding leaders have pursued scale as a strategic objective. Yet amid a new array of market-level uncertainties, including global trade disputes, chronic labor capacity mismatches and economic volatility, the industry’s largest operators continue to demonstrate advantages in purchasing leverage, access to capital, technology investment, land acquisition and operating efficiency that remain difficult for smaller competitors to replicate.

The Berkshire acquisition raises an important benchmark to consider. Perhaps 20,000 annual closings is not merely a growth target but a strategic minimum threshold, a point at which scale begins generating advantages substantial enough to reshape competitive positioning. If that proves true, Berkshire has acquired a platform capable of achieving a different level of scale altogether.

Betting on housing

The third and perhaps underappreciated dimension of the transaction concerns Berkshire Hathaway’s broader view of housing itself.

Historically, homebuilding acquisitions have tended to come from predictable buyers. Another public homebuilder. A privately held builder seeking expansion. Or, increasingly over the past decade, a Japanese housing enterprise seeking a stronger U.S. presence.

This transaction broadens that universe.

“I think it broadens the buyer groups,” Oppenheim observed. “Many people would have thought about buyers being either another homebuilder or a Japanese parent company. This is another path and another source of capital for these acquisitions.”

That statement may be among the most important takeaways from the entire deal.

Berkshire Hathaway is not a homebuilder. It is one of the world’s most sophisticated capital allocators. Its decision to deploy tens of billions of dollars into a homebuilding platform signals confidence in the long-term outlook for housing demand that extends well beyond the current cycle.

The acquisition suggests that large-scale investors increasingly view housing not as a cyclical trade but as a durable long-term operating business tied to fundamental demographic demand.

In that sense, the transaction aligns with broader trends already emerging across the residential landscape, where institutional capital has flowed steadily into rental housing, land development, mortgage finance, and housing-related infrastructure.

Betting on an integrated housing ecosystem

Yet the most intriguing aspect of the transaction may be what it says about Berkshire Hathaway’s evolving position in housing. Because Berkshire is not entering the sector. It is expanding within it.

Through Clayton Homes, Berkshire already controls one of the nation’s largest housing manufacturing and distribution networks. Through businesses such as MiTek, Acme Brick, Johns Manville, Benjamin Moore, Shaw Industries, HomeServices of America, and a range of insurance and financial services operations, Berkshire already participates in multiple stages of the housing value chain.

The acquisition of Taylor Morrison adds something Berkshire previously lacked at scale.

A premier site-built homebuilding platform. That observation invites a larger strategic question.

Is Berkshire Hathaway simply acquiring a homebuilder? Or is it quietly assembling a housing ecosystem?

The Japanese housing enterprises that have expanded aggressively in the United States over the past decade have largely pursued a similar logic. They have sought to integrate development, manufacturing, distribution, construction, and capital into increasingly connected operating systems.

Berkshire’s portfolio increasingly resembles a distinctly American version of that same concept.

Whether intentionally or not, the company now possesses many of the building blocks necessary to influence multiple stages of the homeownership journey.

From financing and insurance to materials, components, construction, brokerage, and now large-scale site-built production.

Avila believes one of the most intriguing unanswered questions concerns what integration may ultimately look like across Berkshire’s housing operations.

“It will be interesting to see how consolidation and integration will look across the Clayton site-built subsidiaries,” he said. “Greg Abel noted the potential to combine operations over time, unlocking synergies that would continue to propel the business toward becoming a national homebuilder.”

Whether those synergies emerge through purchasing, capital deployment, land acquisition, technology platforms, building products, distribution networks, or other operational capabilities remains to be seen.

The observation nonetheless raises an important possibility: Berkshire may not merely own housing businesses. It may increasingly operate them as a coordinated housing enterprise.

The real signal

If Berkshire Hathaway’s acquisition of Taylor Morrison signals anything, it may indicate that demand for high-performing homebuilding platforms – public or private – has never been stronger, and the potential acquirer group has never been as deep nor as varied.

Strategic operators. Global housing and real estate companies. Private-equity-backed platforms. Institutional capital providers. Capital-flush regional private homebuilding fast-trackers.

And now Berkshire Hathaway.