May 26, 2026 — Bond strategists at ING Bank NV, Goldman Sachs Group Inc., Barclays Plc and Deutsche Bank AG warned Sunday that the sharp rise in long-term Treasury yields triggered during the U.S.-Iran conflict is unlikely to meaningfully reverse even if the war ends, signaling what many on Wall Street increasingly view as a structural reset in global borrowing costs rather than a temporary oil-shock distortion.

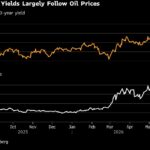

The benchmark 10-year Treasury yield traded near 4.67% late last week — its highest level since January 2025 — after beginning the year below 4%. The 30-year Treasury bond yield climbed above 5.17%, approaching levels last seen before the 2008 financial crisis, while sovereign yields across Europe and Japan have moved sharply higher in parallel.

The message emerging from strategists is increasingly clear: the bond market’s problem is no longer just inflation. It is confidence.

In a Bloomberg analysis published Sunday, strategists argued that “real yields” — Treasury yields adjusted for inflation expectations — are now driving most of the selloff, suggesting investors are demanding materially higher compensation to finance swelling government deficits, escalating defense spending, heavy AI-related debt issuance and the growing possibility that the Federal Reserve under new Chair Kevin Warsh could still raise rates later this year rather than cut them.

“The argument that duration is selling off globally due to inflation fears is hard to square with market pricing of medium- and long-term inflation risk,” wrote Jonathan Pingle in commentary cited by Bloomberg, framing the move as a deeper repricing of fiscal and policy risk rather than a short-term energy spike.

At Goldman Sachs, Phillip Lee, head of real-money rate sales, said on a firm podcast that persistent deficits, expanding Treasury issuance and rising concerns over debt sustainability are increasingly forcing investors to demand higher compensation for holding long-dated government bonds.

“I think rates are going higher,” Lee said bluntly.

The shift marks a major change in how Wall Street is interpreting the bond market. Earlier in the Iran conflict, many investors viewed rising yields primarily as a response to surging crude prices and inflation fears tied to disruptions in the Strait of Hormuz. Increasingly, strategists believe the war merely accelerated pressures that were already building beneath the surface.

Ajay Rajadhyaksha, global chairman of research at Barclays, warned that the forces now driving the bond selloff are not temporary.

“Fiscal deterioration, defense spending, sticky inflation and central bank paralysis are not resolving next week,” Rajadhyaksha wrote. “They are getting worse.”

That view directly clashes with the more optimistic outlook being advanced by Treasury Secretary Scott Bessent, who told Reuters during last week’s G7 finance meetings in Paris that elevated inflation and bond yields remain “transient” and should ease once the conflict subsides.

Bessent argued oil markets themselves are signaling expectations for eventual stabilization, pointing to Brent crude trading near $105 for near-term delivery but closer to $88 for December contracts.

“I think headline will be high as long as the conflict’s going,” Bessent said. “I don’t think that will leak into core through three or four months out.”

Markets increasingly appear unconvinced.

Traders who entered 2026 expecting multiple Federal Reserve rate cuts have rapidly reversed course. Interest-rate futures now imply rising odds of at least one Fed hike before year-end despite slowing portions of the economy and leadership changes at the central bank.

Jim Reid, research strategist at Deutsche Bank, described the recent bond-market move as “aggressive,” while separate Deutsche Bank analysis warned yields could climb even higher if the U.S.-Israeli conflict with Iran triggers further economic disruption or prolonged fiscal spending increases.

A second major driver now compounding the selloff is the artificial-intelligence investment boom reshaping corporate capital markets.

While AI is widely expected to improve long-term productivity, strategists increasingly believe its near-term economic impact is inflationary. Technology giants including Microsoft, Meta Platforms, Alphabet, Amazon and Oracle are collectively spending hundreds of billions of dollars on AI infrastructure, data centers and semiconductor capacity — much of it financed through bond markets already absorbing historically large Treasury issuance.

The result is an extraordinary simultaneous demand for capital from both governments and corporations.

Stronger AI-driven economic growth could also reinforce higher yields by encouraging investors to favor equities over fixed income, forcing bond markets to offer increasingly attractive returns to remain competitive.

At the same time, sovereign debt burdens continue worsening across much of the developed world.

The U.S. federal deficit remains near record peacetime levels even before accounting for war-related military spending and higher interest costs. Treasury issuance is projected to continue climbing into 2027, while major economies including the United Kingdom, Japan, Germany and France face similar financing pressures.

Strategists increasingly believe the traditional buyer base — foreign central banks, commercial banks and institutional asset managers — is no longer willing to absorb that volume of debt at prior yield levels.

That repricing is beginning to ripple far beyond Wall Street trading desks.

Long-term Treasury yields directly influence mortgage rates, auto loans, corporate borrowing costs, credit-card refinancing and small-business lending across the U.S. economy. Mortgage rates have already resumed climbing alongside the 10-year yield, worsening affordability pressures throughout the housing market and placing additional strain on consumers already contending with elevated insurance, transportation and food costs.

For the Trump administration, the bond market is increasingly becoming the central economic constraint.

The White House’s hope that a diplomatic resolution with Iran could rapidly cool inflation and stabilize markets now collides with a growing strategist consensus that long-term borrowing costs are rising for deeper structural reasons that no ceasefire alone can solve.

If that view proves correct, the American economy may remain trapped in a world of elevated financing costs well into 2027 — regardless of what happens next in the Strait of Hormuz.

JBizNews Desk

© 2026 JBizNews. All Rights Reserved. Reproduction or distribution without written permission is prohibited.