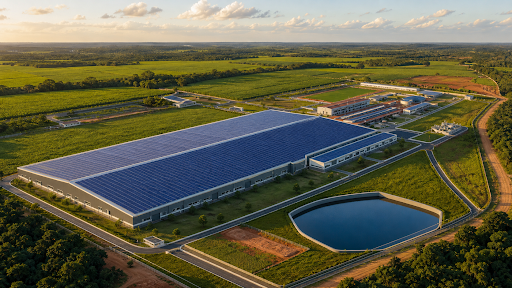

Photo: Proposed layout of Homerun’s planned solar glass manufacturing complex in Bahia, Brazil showing a rooftop-solar-equipped plant and surrounding farmland.

Disseminated on Behalf of: Homerun Resources Inc.

- Homerun’s Bankable Feasibility Study assigns a base-case net present value of USD$670 million and an internal rate of return of 20.2 per cent to what is positioned as the first dedicated solar pattern glass plant in the Americas.

- The 1,000 tonne-per-day Belmonte, Bahia facility targets a Brazilian solar market that imported 17.9 gigawatts of photovoltaic modules in 2025 with no domestic solar glass producer to supply it.

- With letters of intent (LOIs) for roughly 380,000 tonnes per year against plant capacity of 288,300 tonnes, Homerun enters its financing phase with demand visibility above run-rate output.

Brazil is Latin America’s largest solar market, and yet it produces none of its own solar glass. That mismatch defines one of the cleanest first-mover openings in the Americas’ energy transition.

The country imported 17.9 gigawatts of photovoltaic modules in 2025. Roughly 79 per cent went to rooftop and distributed generation. Every panel relies on imported glass moving through 60–90-day Chinese supply chains exposed to tariffs, freight inflation and the long rationalization underway in China’s own solar sector.

That is where Homerun Resources Inc. (TSXV:HMR) (OTCQB:HMRFF) (FSE: 5ZE) (BDR: HMRN31) now finds itself. The Vancouver-based materials company controls the Santa Maria Eterna silica sand district in Belmonte, Bahia, a low-iron, high-purity deposit that feeds a four-vertical strategy spanning industrial silica, solar glass manufacturing, long-duration thermal energy storage and AI-enabled energy management. The solar glass plant sits at the center of that platform, and on May 12th, 2026, the company released a Bankable Feasibility Study confirming the economics of the build.

“Completion of this Bankable Feasibility Study marks a transformational milestone for Homerun and provides a clear technical and financial blueprint for the development of what is intended to be Brazil’s first solar glass manufacturing operation,” —Brian Leeners, CEO of Homerun Resources.

From Validation To A Bankable Number

Before the BFS landed, the Homerun story rested on a thesis that had yet to be quantified: a world-class silica resource paired with the Americas’ missing manufacturing link. The BFS, prepared by Germany-based engineering firm, DTEC PMP GmbH, replaces that thesis with hard numbers.

The base case shows a net present value of USD$670 million, an internal rate of return of 20.2 per cent against a weighted average cost of capital of 4.6 per cent, and an estimated payback of 7.6 years inside a 13-year operating life. Total initial capital expenditure comes in at USD$396.5 million, net of VAT and local taxes.

Indicative gross margins reach approximately 50 per cent at projected 2030 domestic pricing of USD$1,033 per tonne, against unit costs of USD$520 per tonne. By 2033, when the plant reaches full …

This post was originally published here