The U.S. natural gas market is showing signs of seasonal normalization, with the front-month April contract (J26) trading near the lower end of its historical range. While a moderate winter premium remains visible in the Z26 contract, the overall forward curve has moved closer to 2024–2025 levels, reflecting reduced concerns over acute shortages.

Inventories are building faster than average (+56 BCF forecast), pushing storage levels above seasonal norms at around 1.92 TCF. European storage remains tight at just 28.6%, but weather-driven demand is expected to stay near normal in the coming weeks. The supply-demand balance is shifting toward a moderately bearish bias in the short term, although the number of days of supply from storage (16.2 days) continues to provide some underlying support.

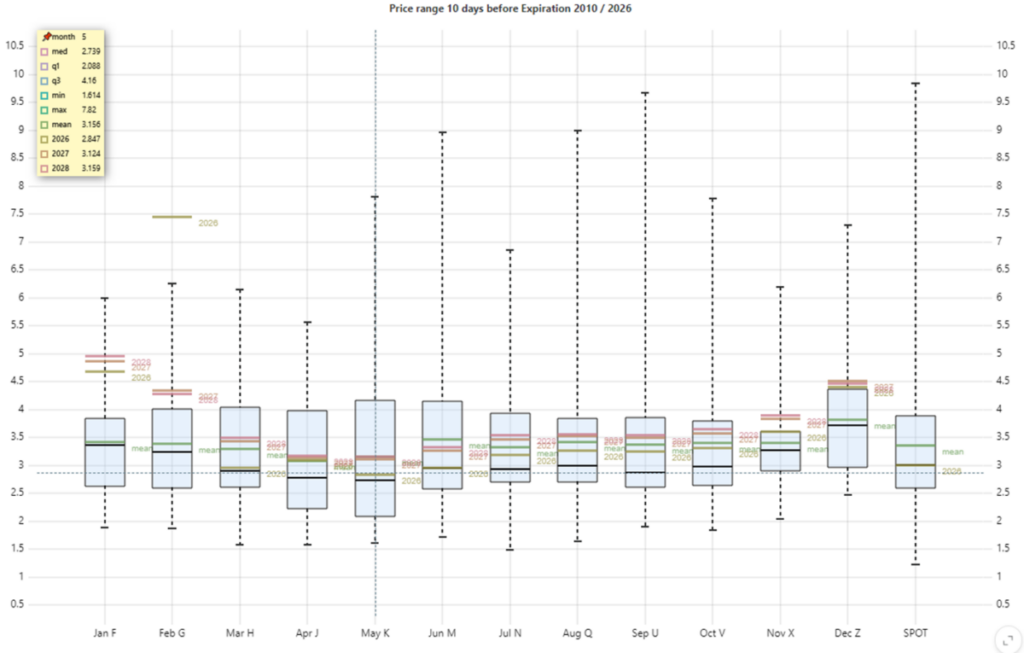

Current natural gas prices compared to the price range 10 days prior to expiration, by month, since 2010

The current price of the nearest April contract (J26) is near the lower end of the historical range for the 10-day period leading up to expiration and is close to the median values. For the summer months, the 2026 curve is generally around the median or slightly below it, with no significant weather premium. The most notable upward deviation persists in the winter contract Z26, which is trading above the average level and closer to the upper half of the historical range. For 2027 and 2028, values are also slightly higher than 2026 in the winter segment, but without an extreme deviation from historical data. Overall, the near end of the curve now looks noticeably calmer than in winter, and the market premium is concentrated mainly in the coming heating season.

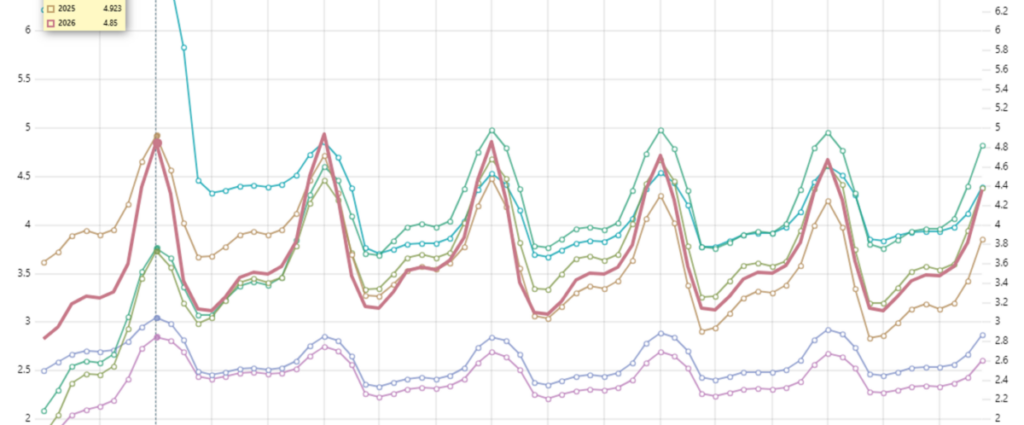

Forward natural gas curve compared to 2020–2026

The 2026 forward curve is significantly lower than the 2022–2023 peaks and, overall, closer to the 2024–2025 trajectory. After the winter peak, the market moves into a range of around 3.7–4.0 during the summer months and then resumes seasonal growth heading into the winter of 2026/27. January 2027 remains one of the most expensive points on the curve, but no longer appears extreme compared to the crisis years. The distant segments for 2028–2030 maintain a stable seasonal sine wave without sharp spikes, which suggests a normalization of long-term expectations. Overall, the current curve reflects a moderate …

This post was originally published here