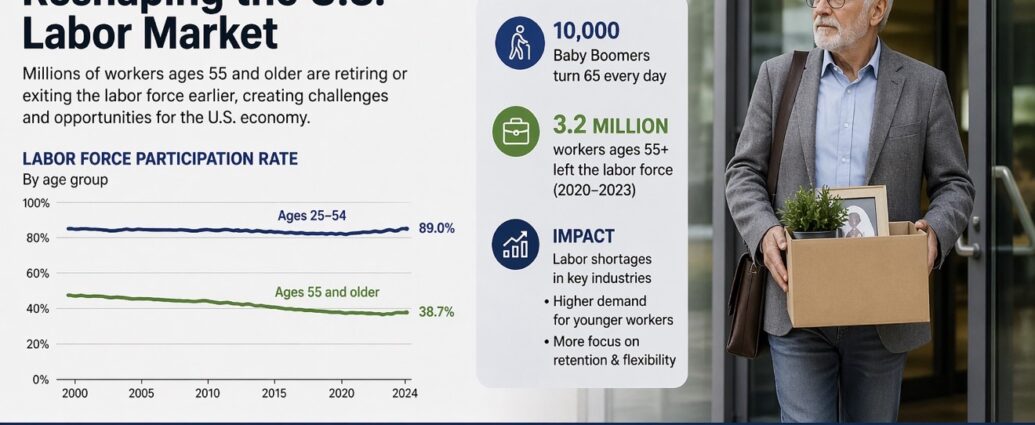

The U.S. labor market is changing in a way that goes beyond immigration and hiring cycles: older Americans are stepping out of work in growing numbers, tightening labor supply and altering the outlook for employers, consumers and policymakers. The latest employment data from the Bureau of Labor Statistics show labor-force participation among people 55 and older remains well below its pre-pandemic trajectory, and Federal Reserve Bank of Kansas City economists said in research on pandemic-era retirements that “excess retirements” became a meaningful drag on labor-force growth, according to the bank’s published analysis.

The demographic force behind that shift is straightforward. In projections published by the Bureau of Labor Statistics, the agency said the labor force “will continue to age,” with workers 65 and older making up a larger share of the workforce through the decade as the population itself gets older. At the same time, the youngest members of the baby-boom generation have entered their 60s, and that transition matters because, as Brookings Institution economist Wendy Edelberg said in labor-market commentary, aging alone “puts downward pressure on participation,” a point echoed in public analysis from several labor economists.

Not all of the decline reflects weak demand for older workers. A sizable share appears tied to financial capacity and lifestyle choice. Federal Reserve Chair Jerome Powell said in earlier remarks on the post-pandemic labor market that retirements had risen and that asset gains likely played a role, a view reinforced by Federal Reserve Bank of St. Louis research linking stronger household balance sheets to earlier retirement decisions. According to the Federal Reserve’s Survey of Consumer Finances and household wealth data, rising home prices and equity-market gains lifted net worth for many older households, giving some workers more freedom to leave jobs earlier than they once expected.

That financial backdrop helps explain why retirement patterns did not fully reverse even after inflation cooled from its 2022 peak. Fidelity Investments said in its retirement analysis that many older Americans continue to prioritize flexibility and health over maximizing years in the workforce, while Transamerica Center for Retirement Studies reported in survey findings that a meaningful share of older workers retired sooner than planned during and after the pandemic. Catherine Collinson, chief executive of Transamerica Institute, said in the group’s public materials that retirement timing increasingly reflects “a complex interplay” of finances, health and caregiving, rather than wages alone.

Employers, meanwhile, face a more complicated staffing environment than the headline unemployment rate suggests. Nick Bunker, economic research director at Indeed Hiring Lab, said in published labor-market commentary that slower labor-force growth means businesses “can’t count on a rapidly expanding supply of workers,” especially in sectors that long relied on experienced older employees. That challenge shows up acutely in healthcare, transportation, skilled trades and local government, where institutional knowledge matters and replacement pipelines often move slowly, according to reporting from Reuters and the Associated Press on labor shortages tied to retirements.

The trend also intersects with technology in ways that cut both directions. Some economists say automation and artificial intelligence could make it easier for companies to operate with fewer workers, but others argue the transition itself may encourage some older employees to leave rather than retrain late in their careers. Dario Amodei, chief executive of Anthropic, has said publicly that AI will change white-collar work significantly over the next several years, while International Monetary Fund Managing Director Kristalina Georgieva said the technology is set to affect a large share of jobs globally. For older workers, that can mean both opportunity and exit pressure, particularly in administrative and professional roles where software adoption is accelerating.

Public policy adds another layer. Janet Yellen, while serving as Treasury secretary, said repeatedly that labor-force participation remained central to the economy’s long-run growth potential, and Congressional Budget Office projections have warned that slower labor-force expansion will weigh on economic output over time. Immigration can offset some of that pressure, but it does not fully solve the retirement wave now moving through the economy, especially because many occupations losing older workers require specific licensing, experience or local labor-market attachment.

There are signs some retirees could still return under the right conditions. AARP has said in employer guidance and survey work that older Americans often want part-time roles, flexible schedules and less physically demanding work rather than a full return to traditional careers. Jo Ann Jenkins, the organization’s former chief executive, said in public remarks that older workers represent “an untapped resource” if employers adapt jobs to meet their needs. That suggests the participation decline is not simply a one-way exit, but a structural shift toward different forms of work that many companies have yet to accommodate.

For markets and executives, the message is clear: a shrinking pool of older workers could keep wage pressures firmer than expected in some industries even if overall hiring cools, while boosting demand for retirement services, healthcare, wealth management and age-friendly consumer products. The next few years matter because Bureau of Labor Statistics projections and Federal Reserve research point in the same direction: population aging, stronger household wealth and changing work preferences are likely to keep older Americans on the sidelines longer, forcing businesses to rethink hiring, training and productivity strategies as the labor market enters a more constrained era.

JBizNews Desk