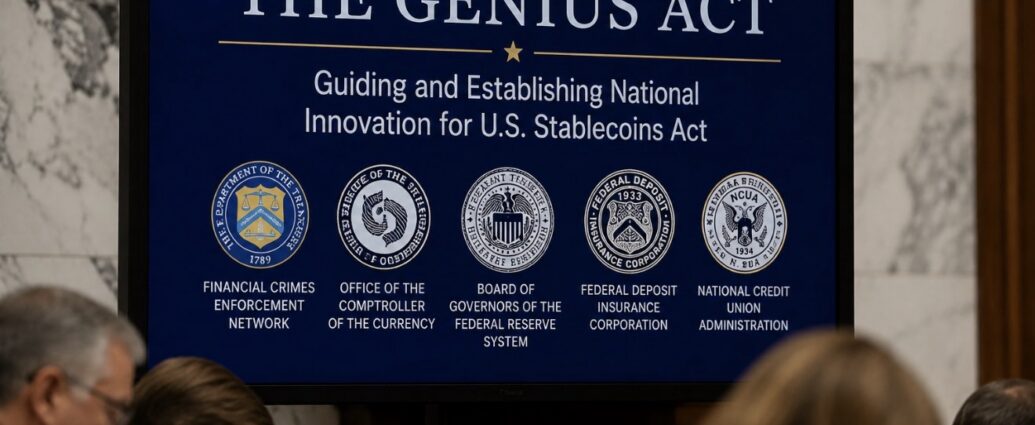

In a joint proposal released on Thursday, June 18, 2026, five federal financial agencies moved to require companies that issue dollar-backed digital tokens to verify their customers’ identities the way banks and credit unions already must. The notice of proposed rulemaking was issued together by the Treasury Department’s Financial Crimes Enforcement Network (FinCEN), the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the National Credit Union Administration.

The rule carries out part of the GENIUS Act — short for the Guiding and Establishing National Innovation for U.S. Stablecoins Act — the 2025 law that created the first federal framework for stablecoins. A stablecoin is a digital token meant to hold a steady value, usually pegged one-for-one to the U.S. dollar and used to move money quickly online. Under the law, licensed issuers — formally called permitted payment stablecoin issuers — are treated as financial institutions under the Bank Secrecy Act, the federal anti-money-laundering statute.

Here is what the proposal would actually require. Each licensed issuer would have to build and maintain a written Customer Identification Program, the same “know your customer” system banks run. Before an account is opened, the issuer would need to collect a customer’s name, date of birth, a physical address, and an identification number — typically a tax ID for U.S. persons, or a passport or similar document for foreign customers — and P.O. boxes and virtual-office addresses would not satisfy the address requirement. Identity records would have to be kept for five years after an account closes.

There is an important limit. The rule reaches only people who deal directly with an issuer — the customers who open accounts and redeem tokens. It does not cover the secondary market. Wallet-to-wallet transfers, trading on exchanges, and other secondary-market transactions would not automatically create customer identification obligations for issuers. Regulators limited the obligations to direct-to-consumer relationships and preliminarily rejected a broader “global” customer due diligence requirement they called unfeasible.

That carve-out is where the disagreement lies. Federal Reserve Board Governor Michael S. Barr said he supports issuing the proposal but warned that the GENIUS Act framework “does not do enough so far to address the risks of illicit finance conducted through secondary market transactions in payment stablecoins.” He said he would carefully review comments on whether parts of the identity rule should be extended to secondary-market activity.

There was also a split at the central bank itself. Five Federal Reserve members voted to approve the proposal, while new Fed Chair Kevin Warsh abstained.

Supporters framed the rule as closing an obvious gap. National Credit Union Administration Chairman Kyle Hauptman said the proposal is the next step to ensure that permitted payment stablecoin issuers are fully integrated into Bank Secrecy Act regulations, adding that it sets clear standards for identifying and verifying account holders and reinforces the commitment to preventing money laundering and terrorist financing.

The push reflects how large the stablecoin market has grown. Dollar-pegged tokens now move billions of dollars a day and have become a real piece of the payments system, used by crypto traders, shoppers, and businesses settling cross-border payments. Because the tokens run on public software networks, people have been able to send large sums across borders in minutes without the identity checks a bank would demand. Crypto-native firms such as Tether, with its USDT, and Circle, with its USDC, have dominated the field, though a number of traditional firms have pushed in as well.

The GENIUS Act sets other guardrails already written into the law. Issuers must hold 1:1 reserves in cash and short-dated U.S. Treasuries, publish monthly disclosures, and cannot pay yield to holders.

The timeline is the part most likely to be misread. The proposal will be open for 60 days following its planned publication in the Federal Register on June 22. The agencies then have to weigh the feedback before issuing final rules, and final customer-identification rules are not expected before 2027. The GENIUS Act itself becomes effective on the earlier of January 18, 2027, or 120 days after the primary federal regulators issue their final rules — meaning the law could switch on before its customer-identity machinery is fully in place.

For the companies caught in the middle, the message is to start preparing now. Building a bank-grade identity system takes time, and issuers face a compressed window of roughly seven months between this proposal and the law’s outside effective date to rebuild how they sign up and verify customers.

JBizNews Desk | Washington

© JBizNews.com All Rights Reserved. Reproduction or distribution without written permission is prohibited.