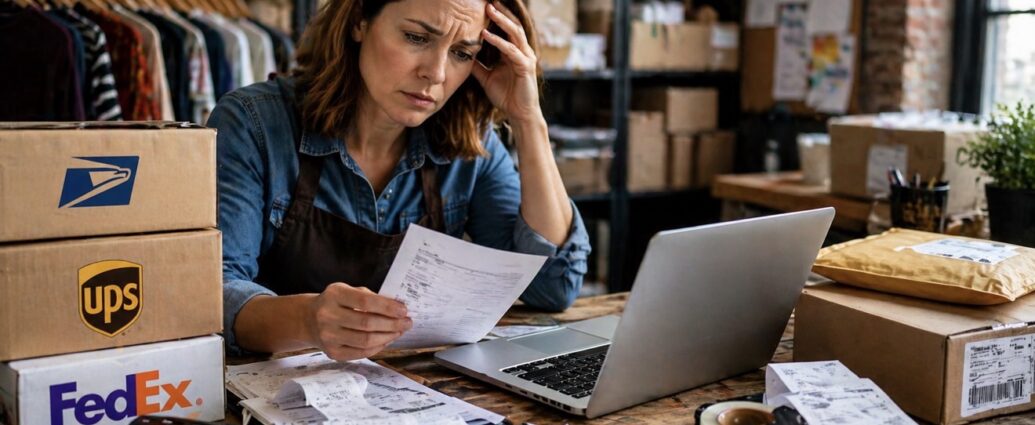

American small retailers are absorbing a punishing convergence of rising shipping costs and a stubborn labor shortage, a double squeeze that is eating into margins at a moment when consumer confidence is running near record lows and tariff uncertainty continues to cloud forward planning.

The most immediate blow came this week. USPS imposed a temporary 8% surcharge on package shipping rates effective April 26, applying to Priority Mail Express, Priority Mail, USPS Ground Advantage, and Parcel Select — the core services that millions of independent retailers and e-commerce sellers depend on daily.  The move is historic: USPS had historically avoided fuel surcharges, relying instead on periodic base rate increases approved by regulators. By adopting a dynamic surcharge model, the agency is signaling a shift toward more market-driven pricing — an approach long used by private carriers.

The timing landed hard for small operators. The surcharge follows a general rate increase of up to 7.8% that already hit in January 2026. For a standard 2-pound package sent via Ground Advantage, the new surcharge adds roughly $1.00 per shipment — and for high-volume, low-margin sellers, the threat to profitability is one many will have no choice but to pass to the end consumer.

The pressure extends well beyond USPS. UPS and FedEx are on pace for a third consecutive record quarter of parcel shipping costs, stacking higher fuel surcharges on top of accumulated general rate increases. A five-pound package shipped via ground from Atlanta to a residential address in New York City cost $22.52 in 2022 compared to $31.94 in 2026 — a 42% increase against cumulative inflation of just 15% over the same period.  The fuel surcharge component alone has driven the bulk of that gap. Surcharges now account for roughly 33% of the average package cost, making them a significant portion of total shipping spend — and for brands shipping oversized or heavy products, a 5–7% base rate increase can easily translate into a 10–18% total cost increase once all fees are factored in.

The root driver is geopolitical. The Strait of Hormuz — a 21-mile-wide waterway carrying roughly 20% of the world’s daily oil supply — has been effectively closed to commercial shipping since late February 2026, sending Brent crude surging past $100 per barrel for the first time in four years. Major container carriers including Maersk, CMA CGM, Hapag-Lloyd, and MSC have suspended transits through the strait and rerouted vessels around the southern tip of Africa, adding 10 to 14 days per shipment.  Those added voyage costs are flowing downstream to every retailer that ships a box.

Parcel consultant Nate Skiver has advised shippers to negotiate fuel surcharge discounts, rate caps, or custom surcharge tables, and to consider switching to alternative carriers where possible. Larger shippers have sufficient leverage to secure concessions that small-to-medium customers simply cannot obtain.  That asymmetry is the crux of the problem for independent retailers — they absorb rate increases at full cost while their large-chain competitors negotiate around them.

On the labor side, the picture is no easier. NFIB’s March survey found that 32% of small business owners reported job openings they could not fill — above the historical average of 24% — with NFIB Chief Economist Bill Dunkelberg noting that small businesses “continue to face difficulties related to labor cost and quality.”  Fifteen percent of small business owners cited labor quality as their single most important problem in March, above the historical average of 12%, while 10% cited labor costs as their single most important problem — a figure that has been gradually climbing.

For many small and mid-sized businesses, the combination of tariff uncertainty, labor regulations, and operating cost volatility is making it harder to forecast — leading to delayed hiring decisions and a preference for flexibility over expansion.  The result is a Main Street caught between two operating constraints at once: too costly to ship, too difficult to staff.

Small businesses, defined as those with fewer than 500 employees, are being hit harder by higher costs than large ones — and they are responsible for 99% of net new jobs in states like California. Some owners report production cuts of 30–50% as costs compound.  For a sector that is the backbone of American employment, the margin math is becoming increasingly difficult to sustain.

Analysts warn the shipping cost environment may not normalize quickly even if geopolitical conditions ease. AFS Logistics CEO has cautioned businesses to brace for a “new normal” of elevated fuel costs, noting that surcharges are unlikely to roll back quickly once the conflict ends and crude prices drop — and that UPS has restructured its fuel surcharge index so it now declines more slowly as fuel prices fall.

For independent retailers without the scale to negotiate carrier contracts or absorb margin erosion, the options are narrowing: raise prices, cut shipment frequency, shift to local pickup models — or accept that the economics of Main Street shipping have permanently changed.

JBizNews Desk

© JBizNews.com. All rights reserved. This article is original reporting by JBizNews Desk. Unauthorized reproduction or redistribution is strictly prohibited.