Sell-side EPS estimates are 13-15% too low. The defense business is modeled at zero. Three catalysts are converging.

This week’s Wolf Pick: Nokia (NOK)

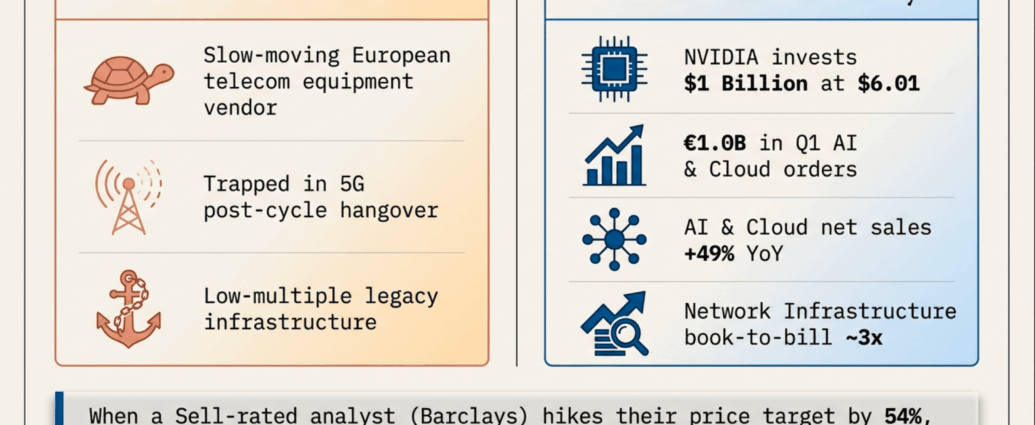

Most people hear Nokia and think of the indestructible brick phone from 2004. Wall Street’s version isn’t much better. Until recently, consensus treated Nokia as a slow-moving European telecom equipment vendor trapped in the 5G spending hangover. That mental model just broke.

Nokia closed Friday at $13.30, a 16-year high. The stock is up roughly 166% over the past 12 months from a 52-week low of $4.00. Three things happened in the last six months that sell-side models haven’t fully absorbed, and they all point in the same direction: Nokia is re-rating from a low-multiple telecom laggard into a credible AI infrastructure name.

The NVIDIA signal and the orders that followed

In October 2025, NVIDIA committed $1 billion of its own balance sheet to Nokia at $6.01 per share. That’s not a strategic press release partnership. That’s real money at a specific price, anchoring Nokia inside NVIDIA’s AI-RAN initiative with T-Mobile for field trials at the end of this year.

Then Q1 2026 earnings landed on April 23 and reset the conversation. According to independent research shared with Wolf Financial, Nokia booked €1.0 billion of AI and Cloud orders in Q1 alone. AI and Cloud net sales grew 49% year over year. Gross margin expanded 320 basis points to 45.5%. Free cash flow jumped 40%. Network Infrastructure book-to-bill (the ratio of new orders to revenue shipped) ran at roughly 3x in AI and Cloud.

The number that matters most is one management revised on the earnings call. At their November Capital Markets Day, Nokia framed its AI and Cloud addressable market as growing at a 16% compound rate through 2028. Five months later, that figure was revised to 27%. The reason: …

This post was originally published here