The punishing global bond sell-off that has rattled markets for the past week paused Tuesday, with U.S. Treasury yields easing modestly even as a closely watched survey of global money managers warned that the 30-year U.S. government bond yield could climb to 6% — a level not seen since late 1999 — as inflation, geopolitical shock and a darkening U.S. fiscal outlook converge on the world’s most important debt market.

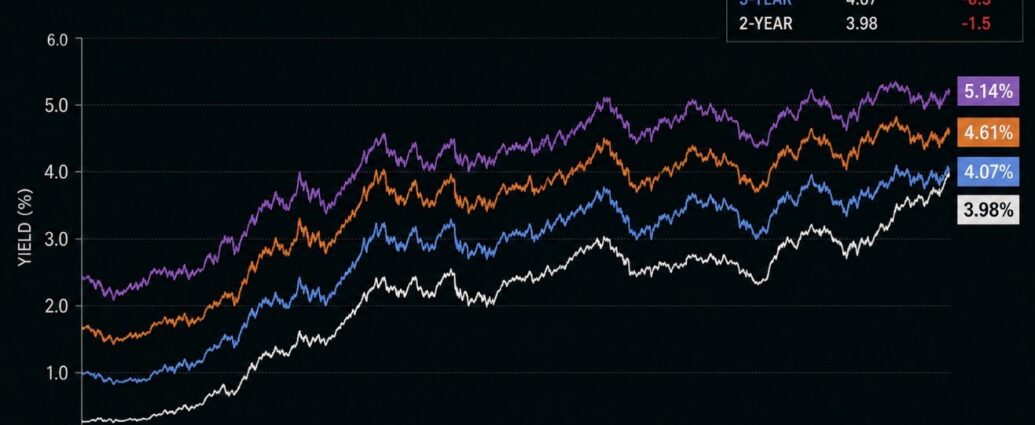

The yield on the 10-year U.S. Treasury note, the global benchmark for borrowing costs that influences everything from mortgages to corporate loans, slipped roughly 1 basis point to 4.6073% in early Tuesday trading after touching its highest level in 15 months during Monday’s session. The 30-year Treasury bond yield held steady at 5.1428%, just below the highest closing level since June 2007. The 2-year note yield, the maturity most sensitive to Federal Reserve policy, fell more than 2 basis points to 4.0695%. One basis point equals one one-hundredth of a percentage point, and bond yields and prices move in opposite directions.

The warning that yields could push significantly higher came from a Bank of America survey published Tuesday, which found that 62% of global fund manager respondents expect the 30-year Treasury yield to reach 6%. That level would mark the highest in more than 26 years and would represent an increase of roughly 86 basis points from current levels. Krishna Guha, vice chairman of Evercore ISI, said in a research note that the combination of rising oil prices, stalled U.S.-Iran negotiations and strong U.S. investment data is putting upward pressure on bond yields globally and creating a new headwind for equities. Subadra Rajappa, head of U.S. rates strategy at Société Générale, told Bloomberg Television that bond yields are starting to feel “unhinged.”

The U.S. story is part of a synchronized global bond rout. Japan’s 30-year government bond yield hit its highest level in history dating back to 1999. The U.K. 10-year gilt yield reached its highest since 2008, and the 30-year gilt yield touched its highest since 1998 as political turmoil swirls around Prime Minister Keir Starmer. German 10-year bund yields climbed to their highest level since May 2011.

What This Means — In Plain English

For readers not steeped in market jargon, here is what is actually happening, explained the way you would discuss it around a dinner table.

When the U.S. government wants to spend more money than it collects in taxes, it borrows. The way it borrows is by selling Treasury bonds. A person, pension fund, bank or foreign government buys the bond and gives the U.S. government cash. In return, the government promises to pay that money back later, plus interest.

The “yield” is essentially the interest rate the government has to offer in order to convince people to lend it money.

When yields rise, it means investors are demanding higher interest payments before they are willing to buy government debt. Right now, that is happening for three major reasons — and all three are hitting simultaneously.

The first is inflation.

If investors believe inflation will remain elevated, they demand more interest because the money they get repaid in the future will be worth less in real purchasing power. Recent U.S. inflation readings have remained stubbornly hot, while oil prices surged above $100 a barrel amid the escalating U.S.-Iran conflict and disruptions near the Strait of Hormuz, one of the world’s most critical energy chokepoints. National gasoline prices have climbed sharply in recent weeks, feeding concerns that inflation may reaccelerate.

The second issue is America’s growing debt load.

The U.S. government is borrowing enormous sums of money to finance deficits. Last week alone, the Treasury Department auctioned roughly $691 billion in Treasury securities. When that much debt floods the market, investors demand better returns to absorb the supply. The more bonds Washington needs to sell, the more attractive yields must become to find buyers.

The third concern is the Federal Reserve itself.

Earlier this year, investors expected multiple Fed rate cuts in 2026 as inflation cooled. But rising oil prices, stronger-than-expected economic data and persistent inflation have forced traders to dramatically rethink those assumptions. Markets are now increasingly pricing in the possibility that the Fed may keep rates elevated longer — and some traders even see a meaningful chance of another rate hike before year-end.

Why It Matters for Everyday Americans

Treasury yields are not abstract Wall Street numbers. They directly shape borrowing costs across the economy.

When Treasury yields rise, mortgage rates usually rise. Car loans become more expensive. Credit-card interest rates increase. Small-business borrowing costs climb. Corporate financing becomes more expensive. Even the federal government itself pays more interest on its debt, worsening deficit pressures further.

The average 30-year fixed mortgage rate climbed back toward 6.65% in recent sessions, according to Mortgage News Daily data, sharply increasing monthly housing costs for buyers already struggling with affordability.

For savers and retirees, higher yields can be beneficial because Treasury bonds and savings products finally offer meaningful interest income again after years of near-zero rates. But for borrowers, the effect is painful.

A higher-rate environment effectively slows economic activity because households and businesses spend more money servicing debt and less money elsewhere.

Why the 6% Level Matters

The last time the 30-year Treasury yield approached 6% was near the end of 1999, before the dot-com bubble collapsed and the U.S. economy entered recession.

Reaching that level again would represent a profound shift in America’s financial environment.

For most of the last quarter century, the U.S. economy has operated under historically cheap borrowing conditions. Low rates fueled home buying, corporate expansion, stock-market growth and massive government deficit spending with relatively manageable financing costs.

A sustained move toward 6% long-bond yields would signal the return of a much more expensive cost-of-capital environment — one many younger Americans have never experienced as adults.

What Wall Street Is Watching Next

Investors are now focused on three major catalysts.

The first is energy markets and whether oil prices continue climbing as tensions with Iran intensify.

The second is upcoming U.S. inflation data, which will heavily influence Federal Reserve policy expectations.

The third is the looming leadership transition at the Federal Reserve itself, with Kevin Warsh expected to assume the Fed chairmanship in the coming weeks. Markets are increasingly trying to determine whether Warsh will prioritize inflation control even at the expense of slower growth, or whether he may tolerate somewhat higher inflation to avoid pushing the economy toward recession.

That decision could shape the trajectory of Treasury yields, mortgage rates, equity valuations and borrowing costs across the global economy for the rest of 2026.

For now, the bond-market sell-off has paused. Whether it resumes may depend less on Wall Street itself than on forces far beyond it — wars, oil prices, inflation, deficits and the next moves from the world’s most powerful central bank.

JBizNews Desk

© JBizNews.com. All rights reserved. This article is original reporting by JBizNews Desk. Unauthorized reproduction or redistribution is strictly prohibited.