America has crossed a fiscal threshold that has not been breached in nearly eight decades. The national debt held by the public has exceeded the total annual output of the United States economy, pushing the debt-to-GDP ratio past 100 percent for the first time since the immediate aftermath of World War II — a milestone that carries real consequences for household budgets, borrowing costs, and the country’s long-term financial standing.

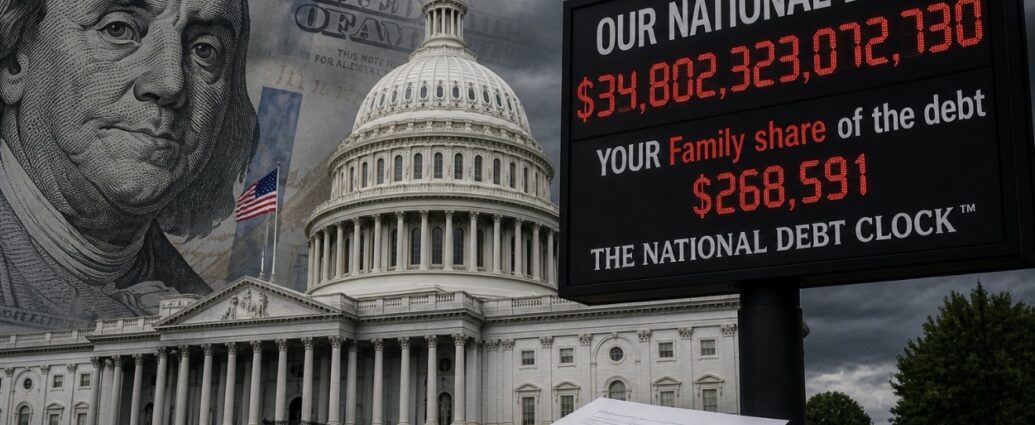

New data released Thursday, April 30, by the U.S. Bureau of Economic Analysis showed that debt held by the public stood at $31.27 trillion as of March 31, while nominal GDP for the 12-month period ending that date was an estimated $31.22 trillion — a gap of roughly $49 billion that pushed the ratio to 100.2 percent. Total gross federal debt, which includes money the government owes to its own trust funds such as Social Security, has already surpassed $39 trillion, a figure that works out to roughly $114,000 per American or $289,000 per household, according to the Senate Joint Economic Committee’s monthly debt update as of April 3, 2026.

What It Means for Everyday Americans

The milestone is not an immediate crisis, but its effects are already being felt. Interest payments on the national debt have surpassed $1 trillion annually — more than the federal government spends on defense, Medicare, or virtually any other program outside of Social Security. For every dollar the government collects in revenue, it spends $1.33, with this year’s deficit projected at approximately $1.9 trillion, according to the Congressional Budget Office.

Maya MacGuineas, president of the Committee for a Responsible Federal Budget, said the milestone carries an unmistakable warning. “We have now borrowed more money than our economy produces in a year,” she told Newsweek. “The debt slows economic growth, pushes up borrowing costs and prices, and leaves us vulnerable to a fiscal crisis in the future. There are good milestones, and bad ones, and this is the worst kind there is.” MacGuineas called the current situation “a total bipartisan abdication of making hard choices,” drawing a sharp distinction from the last time debt reached these levels. After World War II, she said, surging debt was the product of financing the largest military mobilization in American history. Today, it reflects decades of structural spending increases and tax cuts with no offsetting savings.

NPR chief economics correspondent Scott Horsley described the milestone as “the red warning light that’s been flashing for a while now is just a little bit brighter,” noting that crossing 100 percent does not trigger an immediate collapse but does raise the cost of everything from mortgages to car loans as the government competes with private borrowers for available capital.

Not all economists view the threshold as alarming. J.W. Mason, associate professor of economics at John Jay College, City University of New York, told Newsweek the 100 percent milestone was “completely arbitrary” and that there was “no evidence that a country like the United States has any reason to worry about the ratio of debt to GDP.” Douglas Elmendorf, professor of public policy at Harvard University’s Kennedy School of Government and former director of the Congressional Budget Office, similarly said “nothing unusual will happen just because federal debt is passing 100 percent of GDP,” but warned that rising debt means the government “is spending ever more on interest payments,” and if lenders lose confidence, higher interest rates could trigger a “fiscal crisis” and potential “deep recession.”

The Road Ahead

The numbers ahead are stark. The Congressional Budget Office projects the debt-to-GDP ratio will climb to 108 percent by 2030 — surpassing the all-time record of 106 percent set in 1946 — and reach 120 percent by 2036. By 2056, under current trajectories, the ratio could reach 175 percent. The CBO has also warned that by Fiscal Year 2031, the average interest rate paid on federal debt is expected to exceed the rate of economic growth — a condition economists call “R exceeds G” — which, if sustained, can trigger a debt spiral where rising interest costs slow growth and further inflate the debt burden.

The Trump administration has downplayed the debt trajectory, arguing that the president’s economic policies will accelerate growth and naturally reduce the ratio over time. President Donald Trump has regularly cited a goal of 4 percent annual economic expansion. But first-quarter GDP data released alongside the debt figures showed the economy grew at an annualized rate of just 2 percent — an improvement from the 0.5 percent pace in the fourth quarter of 2025, but far below administration targets.

Former South Carolina Governor and United Nations Ambassador Nikki Haley said on X: “America just crossed a dangerous milestone: our national debt now exceeds the size of our economy. When the bill comes due, expect higher taxes, a weaker dollar, fewer services, a weaker military — and our kids stuck paying for it.”

Maya MacGuineas called for a fiscal rule she termed “Super PAYGO” — requiring any new spending or tax cuts to be offset by twice the amount in savings — as a first step. But she acknowledged that stabilizing the debt-to-GDP ratio would ultimately require approximately $10 trillion in total deficit reduction. The Senate adopted a fiscal year 2026 budget resolution last week, a step the Committee for a Responsible Federal Budget called “about a year too late” and one that contains no concrete plan to address the country’s structural deficit.

For American families, the practical consequences are already visible: higher borrowing costs, reduced government flexibility to respond to the next recession or emergency, and an interest bill that now consumes more than 14 cents of every dollar the federal government spends — before a single service is funded or a single road is repaired.

JBizNews-Desk

© JBizNews.com. All rights reserved. This article is original reporting by JBizNews Desk. Unauthorized reproduction or redistribution is strictly prohibited.