Walmart’s latest quarterly results delivered strong top-line numbers — but buried inside the data was a signal that should unsettle every retailer in America: the retail giant’s growth is now being driven not by its traditional working-class base, but by households earning over $100,000 a year.

During Walmart’s Q4 FY2026 earnings call, Walmart U.S. President John Furner confirmed that the majority of the company’s market share gains came from higher-income households — a demographic that historically shopped elsewhere.

That shift is not merely a Walmart story. It is a warning flare about the state of the American consumer.

Research from GlobalData Retail shows that nearly 28% of high-income consumers were shopping at discount chains like Walmart in 2025, up from roughly 20% in 2021.  The trajectory is steep — and it tells a story of financial stress spreading up the income ladder.

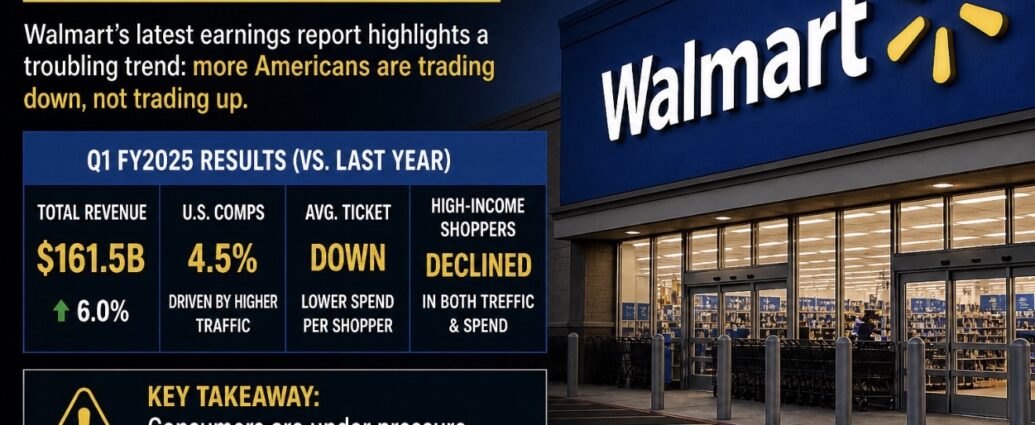

Walmart U.S. comparable store sales rose 4.6% for the quarter, driven by increased customer transactions and unit volumes. E-commerce sales surged 27%, reaching a record-high 23% share of total sales mix. Expedited store-fulfilled delivery grew more than 50%.

Underneath those figures, however, the consumer picture is more sobering. Walmart CFO John David Rainey noted that as household budgets have tightened, more consumer dollars are flowing toward necessities rather than discretionary purchases.  That dynamic — trading down on everything from groceries to general merchandise — is showing up across income brackets, not just at the lower end.

Rainey acknowledged that Walmart has actively worked to broaden its assortment to attract wealthier shoppers, adding roughly 100 new brands in FY2026, including Fender, Kenmore, Weber, and Stanley.  The strategy is working — but it raises a question the company has not fully answered: what happens to the core lower-income shopper who built Walmart into what it is, as the retailer pivots upmarket?

Walmart’s global advertising business expanded 37% during the period, and membership fee revenue climbed 15.1%. Higher-margin digital and advertising segments contributed to a 10.5% rise in constant-currency adjusted operating income, outpacing total sales growth.

The financial mechanics are sound. The social read is more complicated.

When a retailer long considered the definitive barometer of working-class America begins logging its strongest gains from six-figure households, it reflects something deeper than a brand refresh. It reflects an economy in which even comfortable earners are recalibrating — cutting where they can, trading prestige for practicality. Analysts note that if higher-income consumers are pulling back on discretionary spending, the downstream impact on retailers without Walmart’s scale, footprint, and pricing power could be severe.

For smaller retailers, regional chains, and specialty stores that depend on the same mid-to-upper consumer segment now walking into Walmart, the competitive math has shifted. Walmart is no longer just a threat to grocery chains and big-box rivals. It is encroaching on territory once considered safely out of reach.

Walmart raised its full-year net sales outlook to growth of 4.8% to 5.1%, lifted from a prior range of 3.75% to 4.75%, and guided adjusted earnings per share to a range of $2.58 to $2.63.  By every conventional metric, the quarter was a success.

But the more telling metric may be the one Walmart did not highlight in its headline numbers: the accelerating flight of affluent Americans to the discount aisle. That trend, if it holds, will reshape retail competition, consumer brand strategy, and the broader picture of household financial health in America for years to come.

JBizNews Desk

© JBizNews.com. All rights reserved. This article is original reporting by JBizNews Desk. Unauthorized reproduction or redistribution is strictly prohibited.