The company that helped popularize “buy now, pay later” financing wants to become a bank. Klarna, the Swedish financial technology firm whose installment loans have become a familiar option at online checkout pages, has applied for a U.S. national bank charter, a move that would significantly expand its ability to offer savings accounts, payment services, and consumer lending directly to Americans.

The application marks one of the biggest strategic shifts yet for the rapidly growing buy-now, pay-later industry. Rather than relying primarily on partner banks to originate loans, Klarna hopes to operate under its own federal banking charter, allowing it to compete more directly with traditional financial institutions while broadening its product lineup beyond short-term installment financing.

The timing reflects how quickly installment lending has entered the financial mainstream. During this summer’s Amazon Prime Day shopping event, Adobe Analytics estimated that consumers used buy-now, pay-later financing for approximately $2.1 billion in purchases, accounting for 6.6% of all online orders during the promotion. Consumers increasingly view installment payments as another standard checkout option rather than a niche financial product.

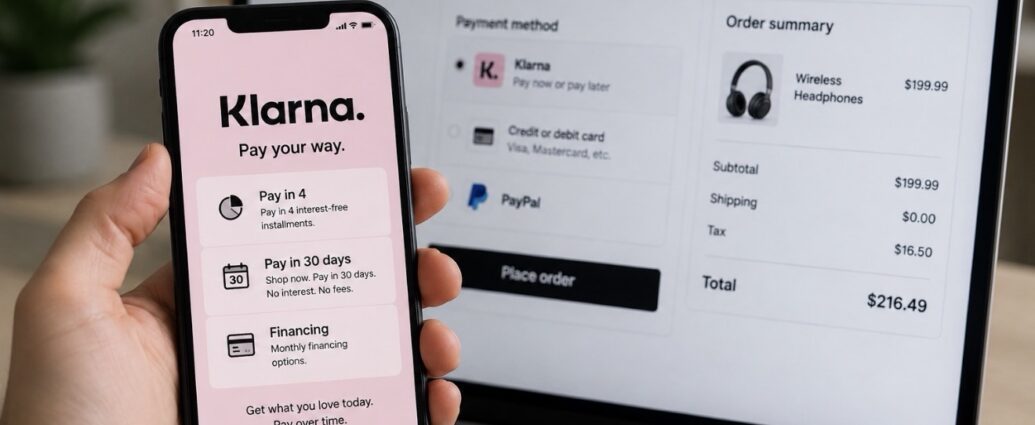

For shoppers, the appeal is straightforward. Rather than paying the full purchase price immediately, customers divide purchases into several smaller payments, often without interest if paid on time. The option has become especially popular for electronics, furniture, home improvement products, travel, and other higher-priced purchases.

A banking charter would allow Klarna to diversify its business beyond installment loans by accepting deposits and expanding consumer banking services. The company already operates banking businesses in parts of Europe, where customers use Klarna for savings accounts, payments, and other financial products in addition to financing purchases.

The move also comes as regulators continue paying closer attention to the rapidly growing buy-now, pay-later sector. Policymakers have increasingly examined disclosure requirements, consumer protections, credit reporting practices, and underwriting standards as installment financing becomes more widely used across retail.

Competition in the industry has intensified. Affirm, Afterpay, PayPal, and several major banks now offer installment-payment products, while many retailers have integrated multiple financing choices directly into online checkout systems. The result has been greater consumer adoption and broader acceptance among merchants seeking to increase sales.

Retailers generally favor installment financing because it encourages larger purchases while reducing shopping-cart abandonment. Consumers who might hesitate to spend several hundred dollars at once are often more comfortable completing purchases when costs are divided into predictable monthly payments.

Consumer advocates, however, continue urging borrowers to exercise caution. While many installment plans carry no interest when paid on schedule, missed payments can trigger late fees, additional charges, and in some cases affect credit histories. Financial experts also warn that managing multiple installment plans simultaneously can become difficult if household budgets tighten.

For the broader financial industry, Klarna’s application underscores the continuing convergence between technology companies and traditional banking. Digital-first financial firms increasingly seek banking licenses to expand services, lower funding costs, and deepen relationships with customers beyond individual transactions.

Whether regulators ultimately approve the charter remains uncertain. Federal banking regulators will review the application through a process that examines capital strength, consumer protections, compliance systems, and the company’s ability to safely operate as a federally regulated financial institution.

Regardless of the outcome, Klarna’s application highlights how dramatically consumer finance has evolved. What began as a simple installment-payment option has grown into a major financial services platform serving millions of shoppers. As digital payments continue reshaping retail, the line separating technology companies from traditional banks continues to blur.

JBizNews Desk | New York

© JBizNews.com All Rights Reserved. Reproduction or distribution without written permission is prohibited.