By JBizNews Desk- Monday, May 4, 2026

For three years, millions of would-be home buyers sat on the sidelines waiting for mortgage rates to fall. By February 2026, it finally looked like their patience was paying off. Then a war changed everything — and something unexpected happened: buyers stopped waiting anyway.

The story of the 2026 spring housing market is one of whiplash, resilience and a quiet but decisive shift in how American buyers are thinking about homeownership. After months of hard-won affordability progress evaporated in a matter of weeks, buyers came back — not because rates dropped dramatically, but because they stopped believing rates ever would.

Nine Months Gone in Weeks

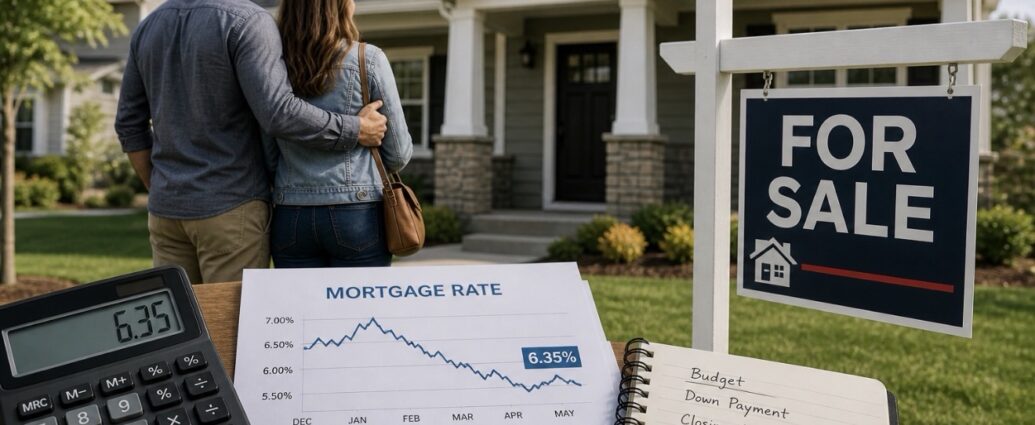

The rate swings have been severe. The 30-year fixed mortgage rate entered 2026 around 6.4%, then fell steadily through January and February, touching 5.99% at the end of February — the first time rates had cracked below 6% in more than three years, according to Mortgage News Daily. It felt like momentum. Then the U.S. and Israel struck Iranian military targets on February 28. Oil prices spiked, 10-year Treasury yields followed, and a single Consumer Price Index reading on April 10 showed inflation jumping from 2.4% to 3.3% in a single month. Nine months of affordability progress vanished in weeks.

Selma Hepp, chief economist at Cotality, put it plainly: “The lesson from this spring is that affordability gains are fragile.”

Purchase applications fell 7% year over year in the week of April 8 — the first annual decline since January 2025 — as buyers paused at the peak of the rate panic. Then something shifted. Applications rebounded 10% week over week and 14% year over year in the week ending April 17, as the 30-year rate eased to 6.35% when financial markets responded to ceasefire talks. Redfin reported up to a 35% increase in offers being written in recent weeks. The number of homes going under contract in March rose 4.6% compared to the prior year, according to Zillow.

Why Buyers Are Coming Back

The buyers returning to the market are not doing so because rates fell dramatically. They are doing so because they have concluded that waiting for meaningfully lower rates is a losing strategy.

On a $400,000 home with 20% down, a 6.35% mortgage means a monthly principal and interest payment of roughly $1,988. At the pandemic low of 3% in 2021, that same payment was about $1,349. The $639 monthly gap is real — and it is not closing soon. But the calculus has shifted. A median-income household can now afford a home worth $30,302 more than a year ago, according to Zillow analysis — a product of rising incomes and slower price growth creating breathing room even as rates have ticked back up.

Nobody credible is forecasting a return anywhere near pandemic-era borrowing costs within the next 12 months. J.P. Morgan’s 2026 housing outlook expects 30-year rates to stay above 6% even with potential Federal Reserve easing later this year. Fannie Mae’s April 2026 forecast pegs the 30-year rate at 6.3% for the second quarter and 6.1% for the rest of the year.

Jordan Del Palacio, a loan partner at Churchill Mortgage, warned that even on good days there is caution built into the rate environment. “We won’t see rates come back down until there is more certainty about a resolution” in the Iran conflict, he said. “If I had to look into my crystal ball, I would probably estimate the average 30-year mortgage rate will be around 6.50% by the end of May.”

The Market Has Shifted in Buyers’ Favor

Even as rates remain elevated, the broader housing market has moved in buyers’ direction in ways that matter. Active inventory nationwide has risen 142.1% since January 2022. Sellers are cutting prices, homes are sitting longer, and builders are offering rate buydowns to move inventory.

Sarah DeFlorio, vice president of mortgage banking at William Raveis Mortgage, expects rates to land between 6.125% and 6.25% by the end of May. “My hope is that during May 2026, we will experience another period of stability, slowly declining rates,” she said. “Sadly, we know from experience it’s never a straight line down.”

Hepp warned that rates could spike again quickly if the next CPI data shows inflation still running hot, oil prices jump or the Iran ceasefire falls apart. “If the 10-year Treasury breaks back above 4.50%, the 30-year mortgage rate will head straight back toward 6.75% or higher, effectively ending the spring homebuying momentum,” she said.

For buyers who came back in April and May, the bet is straightforward: their income supports the payment today, local prices are unlikely to fall significantly, and waiting another year costs more in missed equity and rising rents than it saves in interest. In a market where rates may never return to 3%, that calculation is increasingly hard to argue with.

— JBizNews Desk

© JBizNews.com. All rights reserved. This article is original reporting by JBizNews Desk. Unauthorized reproduction or redistribution is strictly prohibited.