Inflation Panic Sends US Consumer Confidence To All-Time Low: University Of Michigan

Confidence among American consumers has never been this depressed in the history of the University of Michigan survey.

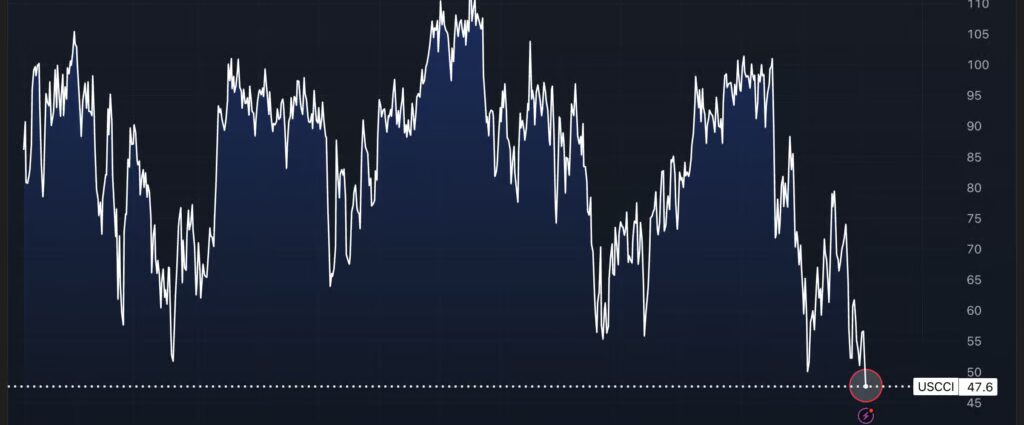

The preliminary April consumer sentiment index crashed to 47.6 — an all-time record low, an 11% monthly plunge and a sharp miss against the 52 consensus — as the Iran war’s economic fallout spread from the gas pump into households’ broader outlook on their finances, jobs and the future.

Chart: Worst Consumer Confidence Reading Since Records Began

Consumer Surveys For April 2026: Full Breakdown

| Indicator | April 2026 | March 2026 | April 2025 | MoM Change | vs. Consensus |

|---|---|---|---|---|---|

| Consumer Sentiment | 47.6 | 53.3 | 52.2 | –10.7% | MISS vs. 52.0 |

| Current Economic Conditions | 50.1 | 55.8 | 59.8 | –10.2% | — |

| Consumer Expectations | 46.1 | 51.7 | 47.3 | –10.8% | — |

| 1-Year Inflation Expectations | 4.8% | 3.8% | 5.3% | +100bps | BEAT vs. 3.8% |

| 5-Year Inflation Expectations | 3.4% | 3.2% | — | +20bps | — |

Iran War Didn’t Raise Prices. It Raised What People Expect Prices To Do

Aside from the shocking sentiment headline in Friday’s data, the inflation expectations component also negatively surprised.

Year-ahead inflation expectations surged from 3.8% in March to 4.8% in April, a 100-basis-point jump in a single month, blowing past the 4.2% consensus and marking the largest one-month increase since April 2025.

The current reading now exceeds every 2024 reading and sits well above the 2.3%–3.0% range that prevailed in the two years before the pandemic.

Five-year inflation expectations ticked up from 3.2% to 3.4%, the highest reading since November 2025 — but held more contained than the short-run surge, a distinction that carries real meaning for the Federal Reserve.

Chart: Americans Expect 4.8% Inflation Next Year Fed Targets 2%