What to Expect When Markets Open Monday After the Iran War Deal

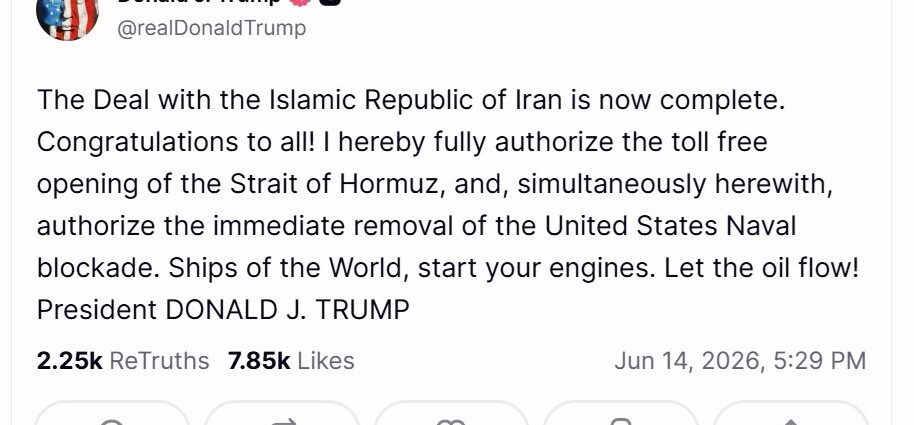

U.S. stock futures jumped and oil prices fell sharply in Sunday evening trading after President Donald Trump announced that the United States had reached a deal with Iran to end nearly four months of war. “The Deal with the Islamic Republic of Iran is now complete,” Trump wrote, adding that he had authorized the reopening of the Strait of Hormuz and the removal of the U.S. naval blockade. “Ships of the World, start your engines. Let the oil flow!”

The announcement triggered an immediate reaction across financial markets that have been whipsawed since the conflict began on Feb. 28.

Futures tied to the S&P 500 rose 0.76% to 7,491.75, a gain of nearly 57 points. Dow Jones Industrial Average futures added 283 points, or 0.55%, to 51,888. Nasdaq futures climbed 1.26%, up 374 points to 30,036.25. Futures on the Russell 2000, which tracks 2,000 smaller American companies, opened at a record high.

Oil, which had carried a significant war premium for months, dropped sharply. Brent crude, the international benchmark, fell 3.8% to below $84 a barrel, its lowest level since early March. West Texas Intermediate, the U.S. benchmark, slid 4.3% to about $81 a barrel.

Elsewhere, gold rose 1.55% to $4,304.60, Bitcoin gained roughly 1.8% to $65,600, and the VIX, Wall Street’s fear gauge, plunged 9% to 17.68, reflecting a dramatic decline in investor anxiety.

The heart of the agreement is the Strait of Hormuz, the narrow waterway through which roughly 20% of the world’s oil supply passes each day. The strait has been effectively closed since the war began, sending shock waves through global energy markets and driving up the cost of oil, gasoline, fertilizer, plastics, packaging materials, and transportation.

The resulting inflation pressures rippled across the broader economy, affecting everything from grocery prices to manufacturing costs.

Trump said the strait would officially reopen Friday, when crews begin clearing mines from the waterway. Even with an order to reopen, analysts caution that restoring normal shipping operations could take weeks or even months. Hundreds of vessels remain stranded on both sides of the chokepoint, and insurance and security costs remain elevated.

Consumers may eventually see relief at the gas pump.

Patrick De Haan, an analyst at GasBuddy, said gasoline prices could fall to roughly $3.75 per gallon by July 4 if the agreement holds and oil continues to retreat. He cautioned, however, that the coming days will be critical in determining whether the ceasefire proves durable.

Before the war, average gasoline prices in many parts of the country were below $3 per gallon. The closure of the Strait of Hormuz and soaring shipping costs pushed prices significantly higher, placing additional strain on households and businesses alike.

The energy shock also contributed to broader inflation concerns. According to the Bureau of Labor Statistics, consumer prices in May were 4.2% higher than a year earlier, marking the sharpest annual increase since April 2023.

Iran publicly confirmed the agreement.

Kazem Gharibabadi, Iran’s deputy foreign minister, said on state television that both sides had agreed to halt hostilities and begin negotiations toward a comprehensive long-term settlement within the next 60 days.

Pakistan’s Prime Minister Shehbaz Sharif also confirmed the agreement, saying preliminary talks would be followed by technical negotiations and ultimately an official signing ceremony.

Still, investors remain cautious.

Markets have repeatedly rallied on reports of diplomatic progress only to reverse course following renewed violence. New warning signs emerged Sunday.

Iran’s semi-official Fars News Agency reported that marine traffic in the Persian Gulf would continue to be regulated jointly by Iranian and Omani authorities, a position that could conflict with Trump’s insistence on unrestricted navigation through the Strait of Hormuz.

Meanwhile, Israeli strikes in Lebanon underscored the fragile nature of regional stability.

Mohammed Bagher Ghalibaf, a prominent Iranian political figure and former Revolutionary Guard commander, argued that the attacks demonstrated that Washington either could not or would not fully enforce the agreement.

The deal arrives ahead of a critical week for financial markets.

The Federal Reserve meets Tuesday and Wednesday for the first policy meeting under new Chair Kevin Warsh, who was sworn in last month as the central bank’s 17th chairman.

Most economists expect the Fed to leave its benchmark interest rate unchanged within the 3.50% to 3.75% range.

Before the agreement, elevated energy prices complicated the inflation outlook and reduced expectations for future rate cuts. With oil prices now falling sharply, some of that pressure could ease.

Warsh, widely viewed as an inflation hawk, has indicated that he may take a different approach from his predecessor, Jerome Powell, including potentially holding fewer post-meeting press conferences. Investors will be looking closely for signals about the central bank’s outlook on inflation, growth, and future interest-rate policy.

“The Kevin Warsh era has begun,” said Phil Camporeale, chief investment strategist at J.P. Morgan Wealth Management, who expects the Fed to remain on hold through the rest of 2026 while adopting a more neutral policy stance.

For now, the market reaction reflects relief after months of uncertainty, military escalation, and economic disruption.

Whether that optimism lasts will depend on two simple questions that markets will answer in the days ahead:

Will oil begin flowing normally through the Strait of Hormuz again?

And will the guns remain silent?

JBizNews Desk

© JBizNews.com All Rights Reserved. Reproduction or distribution without written permission is prohibited.