Trump Names FHFA Chief Bill Pulte Acting Intelligence Director While He Continues Overseeing Fannie and Freddie

By JBizNews Desk

Tuesday, June 2, 2026

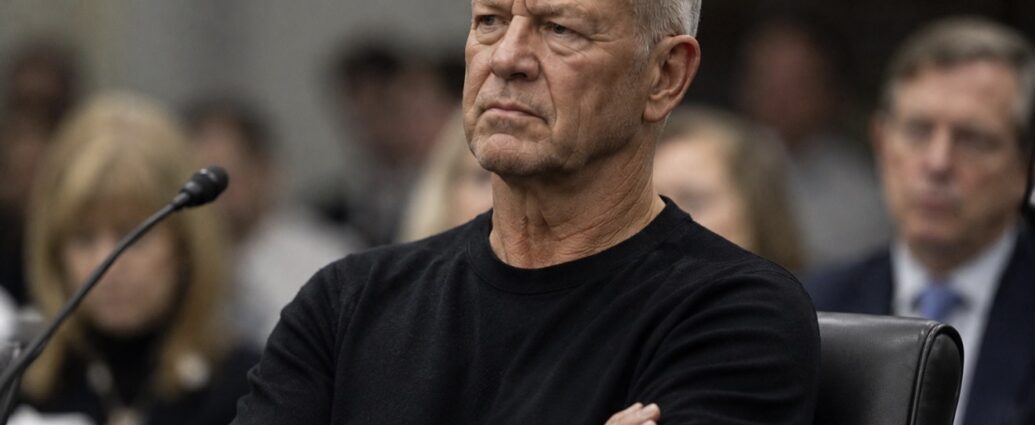

President Donald Trump named Bill Pulte, the director of the Federal Housing Finance Agency (FHFA), as acting director of national intelligence on Tuesday, adding one of Washington’s most sensitive national-security jobs to an official who already oversees America’s housing-finance system.

The development carries implications far beyond politics. In announcing the appointment on Truth Social, Trump said Pulte will continue serving as FHFA director while remaining chairman of Fannie Mae and Freddie Mac, the two government-controlled mortgage giants that collectively support more than $10 trillion in U.S. home loans.

Trump praised Pulte’s management experience and highlighted his stewardship of the housing-finance system, signaling confidence that he can simultaneously oversee both responsibilities.

That unusual arrangement means one official will now oversee the nation’s mortgage-finance infrastructure while also coordinating the work of the U.S. intelligence community.

For homebuyers, lenders, builders, and investors, that is the part of the announcement that matters most.

Many Americans have never heard of the FHFA, but its influence is felt every day throughout the housing market. The agency regulates Fannie Mae and Freddie Mac, which guarantee a significant share of U.S. residential mortgages. Their policies affect mortgage availability, underwriting standards, lender requirements, and ultimately the cost of homeownership.

When Americans obtain a conventional 30-year mortgage, there is a strong likelihood that either Fannie Mae or Freddie Mac will ultimately stand behind the loan.

Since taking office, Pulte, the grandson of the founder of homebuilder PulteGroup, has become one of the most active housing regulators in recent memory.

After being confirmed by the Senate in March 2025, Pulte moved quickly to install new leadership at both Fannie Mae and Freddie Mac while reshaping agency priorities. His tenure has included the termination of several Special Purpose Credit Programs, reductions in diversity, equity and inclusion spending, and the rescission of certain fair-lending and climate-risk guidance issued under previous administrations.

He has also become a central figure in one of the most closely watched debates in housing finance: whether Fannie Mae and Freddie Mac should eventually be released from government conservatorship.

That question has lingered since the 2008 financial crisis and carries enormous implications for lenders, mortgage investors, taxpayers, and the broader housing market. Any move toward privatization would represent one of the largest financial restructurings in modern American history.

Now, the official overseeing that process is taking on a second full-time role.

The position of director of national intelligence is among the most demanding jobs in the federal government. The office coordinates intelligence gathering and analysis across 18 agencies, including the Central Intelligence Agency (CIA) and the National Security Agency (NSA). The role serves as a central hub for national-security assessments involving terrorism, cyber threats, foreign adversaries, and military conflicts around the globe.

Unlike many previous intelligence leaders, Pulte does not come from a military, intelligence, or national-security background, a fact critics immediately highlighted following the announcement.

He succeeds Tulsi Gabbard, who served as Trump’s first director of national intelligence. Gabbard announced plans to depart the role in May amid reports of growing disagreements with the administration.

Pulte has also generated headlines through a series of criminal referrals involving prominent political figures. Those referrals included allegations involving New York Attorney General Letitia James, Sen. Adam Schiff, Federal Reserve Governor Lisa Cook, and former Congressman Eric Swalwell. All denied wrongdoing, and legal outcomes have varied across the cases.

The appointment comes at a particularly sensitive moment.

The United States remains engaged in a broader confrontation involving Iran, while energy markets continue monitoring tensions surrounding the Strait of Hormuz, one of the world’s most critical oil shipping routes. Investors have been closely watching geopolitical developments amid concerns about energy prices, inflation, and global economic stability.

Against that backdrop, a new acting intelligence chief with limited national-security experience adds another variable for markets already navigating uncertainty.

There are also limits on how long the arrangement can continue without Senate action. Under federal vacancy rules, acting officials generally may serve for a limited period while the White House determines whether to nominate a permanent replacement. Any permanent appointment would require Senate confirmation.

For now, there is no immediate indication that Pulte intends to step back from his housing responsibilities.

What This Means for Mortgage Rates

The appointment is not expected to have any immediate effect on mortgage rates or lending standards.

However, investors, lenders, and housing-industry participants will be watching closely to see whether Pulte maintains the same level of focus on FHFA policy while serving in his new role. Markets will also continue monitoring any potential efforts involving the future structure of Fannie Mae and Freddie Mac, an issue that could have significant long-term implications for the U.S. housing-finance system.

For everyday Americans, the takeaway is straightforward: the official with enormous influence over the nation’s mortgage market has just taken on one of the most demanding jobs in Washington. Whether both responsibilities can receive equal attention may become an important question in the months ahead.

Washington — JBizNews Desk

© JBizNews.com All Rights Reserved. Reproduction or distribution without written permission is prohibited.