Why IonQ Stock Is Sliding On Friday?

2026-04-17

IonQ Inc. (NYSE:IONQ) shares are under pressure Friday morning. Nasdaq futures are up 0.20% while S&P 500 futures have gained 0.26%.

After skyrocketing more than 50% this week, the stock is seeing natural profit-taking from investors.

No specific company event triggered the slide, but recent data shows a climb in bearish bets.

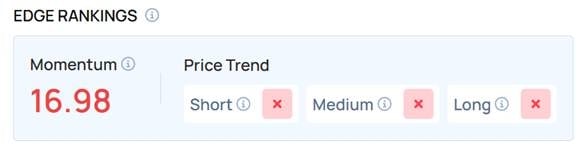

Short interest in the quantum firm rose from 79.48 million to 80.93 million shares during the last reporting period. This currently places 22.78% of the company’s float in short positions.

Sector Momentum and Nvidia Catalyst

The dip comes despite a massive week for the …

This post was originally published here