Gavin Newsom Slams Trump’s ‘Iran War Tax’ As California Gas Price Breaks $6/Gallon Threshold

2026-05-04

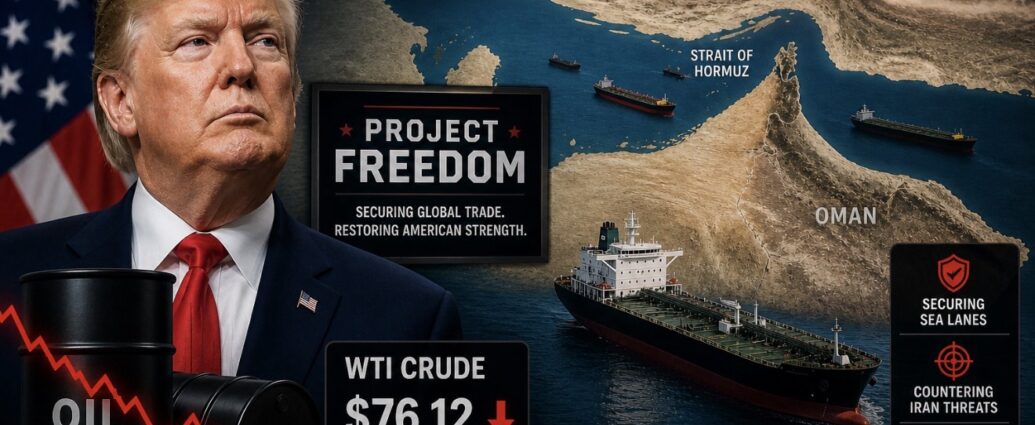

Governor Gavin Newsom (D-CA) slammed President Donald Trump on Saturday as gas prices continued to surge amid escalating tensions in the Middle East due to the ongoing U.S.-Israel and Iran war.

Trump Iran War Tax

In a post on the social media platform X, Newsom’s official Press Office handle delivered sharp criticism of Trump, saying that the war in Iran had “driven U.S. gas prices up 44% to a four-year high.”

data-variant=”card”

data-news-mode=”manual”

>

This post was originally published here