Gas Hits 4-Year High at $4.56 a Gallon as 45 Million Drivers Hit the Road for Memorial Day

If you filled up your tank this weekend, you already know: gas is expensive again.

The American Automobile Association (AAA) said Thursday, May 21, 2026, that the national average price for regular gasoline has climbed to $4.56 a gallon — the highest Memorial Day weekend level in four years and $1.38 more than last year. By Sunday, millions of Americans were feeling it firsthand as a record 45 million people hit the highways for the holiday weekend.

A normal 15-gallon fill-up that cost around $48 last Memorial Day now costs roughly $68.

For families driving from New York to the Jersey Shore, Chicago to a lake house, or Los Angeles to San Diego, that difference adds up fast. A road trip that once felt affordable suddenly costs noticeably more before the vacation even begins.

“Travel demand remains strong, and despite higher fuel prices, many people are prioritizing leisure travel,” said Stacey Barber, vice president of AAA Travel.

People are still traveling. They’ve waited months for the holiday weekend. But many are watching every dollar more closely.

The current national average sits just below the all-time Memorial Day record of $4.61 per gallon, set in 2022 after Russia’s invasion of Ukraine disrupted global oil markets.

This time, the cause is different.

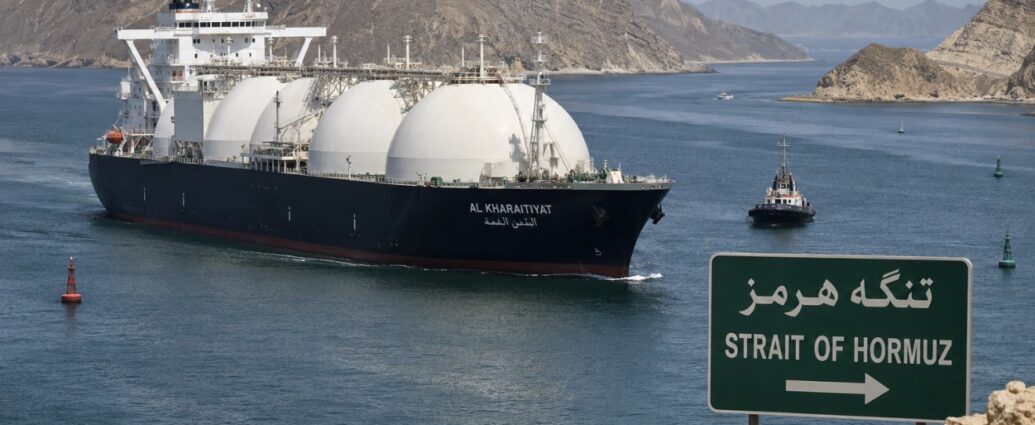

Gas prices have surged more than 50% since late February, when the U.S.-Iran conflict escalated and shipping through the Strait of Hormuz — one of the world’s most important oil routes — became heavily disrupted. Roughly 20% of the world’s oil supply normally passes through the strait, meaning instability there quickly affects fuel prices everywhere.

For the first time in nearly three years, every U.S. state is now averaging above $4 a gallon.

Drivers in California are paying the most, with average prices around $6.14 per gallon, meaning a standard fill-up can cost more than $90. Washington ($5.78), Hawaii ($5.64), Oregon ($5.35), Alaska ($5.27), Nevada ($5.27), Illinois ($5.01), Arizona ($4.81), Colorado ($4.76), and Ohio ($4.76) are also among the most expensive states.

Drivers in the Gulf Coast and Southeast are paying slightly less, though prices are still historically high. Mississippi currently has the cheapest average at $4.01, followed by Georgia, Louisiana, Texas, Oklahoma, Arkansas, Alabama, and South Carolina.

According to GasBuddy petroleum analyst Patrick De Haan, at least 19 states are expected to post record-high Memorial Day gas prices this weekend.

The pain is hitting working families hardest.

Research from Bank of America shows roughly 1 in 10 lower-income households are now spending more than 10% of monthly income on gasoline alone. Economists at Brown University’s Climate Solutions Lab estimate American households have spent an extra $24 billion on gasoline since the Iran conflict began earlier this year — roughly $200 extra per household.

For many families, that money would normally go toward groceries, utility bills, summer camps, or savings.

Americans are already changing habits to cope.

Costco, Sam’s Club, BJ’s Wholesale Club, Walmart, and Kroger discount fuel stations are seeing heavier traffic as drivers search for cheaper prices. Gas price apps are surging in popularity. More commuters are carpooling, combining errands, or working remotely extra days to avoid filling up as often.

Some families are shortening vacations altogether, replacing longer road trips with closer regional getaways.

Small businesses are under pressure too.

Contractors, landscapers, delivery drivers, plumbers, electricians, rideshare drivers, and trucking companies are all absorbing sharply higher fuel costs. Many are adding fuel surcharges or raising prices, which then pushes costs higher across the broader economy — from food delivery to home repairs.

Industry analysts warn prices may climb further.

GasBuddy projects the national average could approach $4.80 per gallon during peak summer travel season. If tensions in the Middle East worsen or the Strait of Hormuz remains partially closed deep into the summer, analysts say the all-time U.S. record of $5.02 per gallon set in June 2022 could come back into play.

The U.S. Energy Information Administration says gasoline demand is still rising while inventories are tightening, leaving little room for additional supply disruptions.

There is one possible relief valve.

The Trump administration is currently engaged in negotiations with Iran through mediators in Oman and Pakistan, and reports this weekend suggest Tehran may agree to surrender part of its enriched uranium stockpile as part of a broader agreement that could reopen the Strait of Hormuz.

If a deal is finalized, oil prices could fall quickly — and gasoline prices would likely follow. If negotiations collapse, drivers could face another leg higher at the pump.

For now, AAA says travelers should plan carefully: fill up in cheaper states when possible, monitor gas-price apps, avoid speeding, and check tire pressure to improve fuel economy.

For millions of Americans heading home from the holiday weekend, one thing is clear: the Iran conflict is no longer just a geopolitical story happening overseas. It is now directly shaping household budgets across the country every time drivers stop for gas.

— JBizNews Desk

© 2026 JBizNews. All Rights Reserved. Reproduction or distribution without written permission is prohibited.